Texas mortgage laws are unique because the state embeds its home equity lending rules directly into its Constitution, creating some of the strictest homeowner protections in the country. Under Article XVI, Section 50(a)(6), every rule governing home equity borrowing carries constitutional weight. That means changing any provision requires a statewide voter referendum, not just a legislative vote. The Texas Finance Commission and the Texas Credit Union Commission oversee compliance, but the constitutional foundation sets the floor. This guide explains why Texas has unique mortgage laws, what those rules mean for borrowers and lenders, and how to work within them effectively in 2026.

Why Texas has unique mortgage laws: the constitutional foundation

Texas did not always allow home equity lending. Home equity lending became legal in Texas only on January 1, 1998, making it the last state in the country to permit it. Lawmakers and voters chose to legalize it only after embedding strict consumer protections directly into the state Constitution. That decision defines everything about Texas mortgage regulations today.

The governing provision is Article XVI, Section 50(a)(6) of the Texas Constitution. Every rule about who can lend, how much they can lend, and under what conditions flows from this single constitutional section. No legislature can quietly amend it between sessions. Any change requires a statewide referendum, which means Texas housing laws stay stable across political cycles in a way that statutory rules in other states simply do not.

This constitutional structure creates a meaningful contrast with other states. In most states, home equity lending rules are statutory. A legislature can revise them with a simple majority vote. In Texas, the constitutional nature of these protections makes them far harder to erode, offering long-term stability for both borrowers and lenders who build compliance programs around them.

Key features of the constitutional framework include:

- Home equity lending was legalized in 1998 via constitutional amendment

- All rules are governed by Article XVI, Section 50(a)(6)

- Changes require a statewide voter referendum

- Oversight shared by the Texas Finance Commission and the Texas Credit Union Commission

- Protections apply to primary residences only, not investment properties

What are the key consumer protections in Texas home equity law?

Texas home equity law packs more borrower protections into a single constitutional section than most states manage to fit into entire statutory codes. These protections are not optional guidelines. They are hard legal requirements, and lenders who miss them face severe consequences.

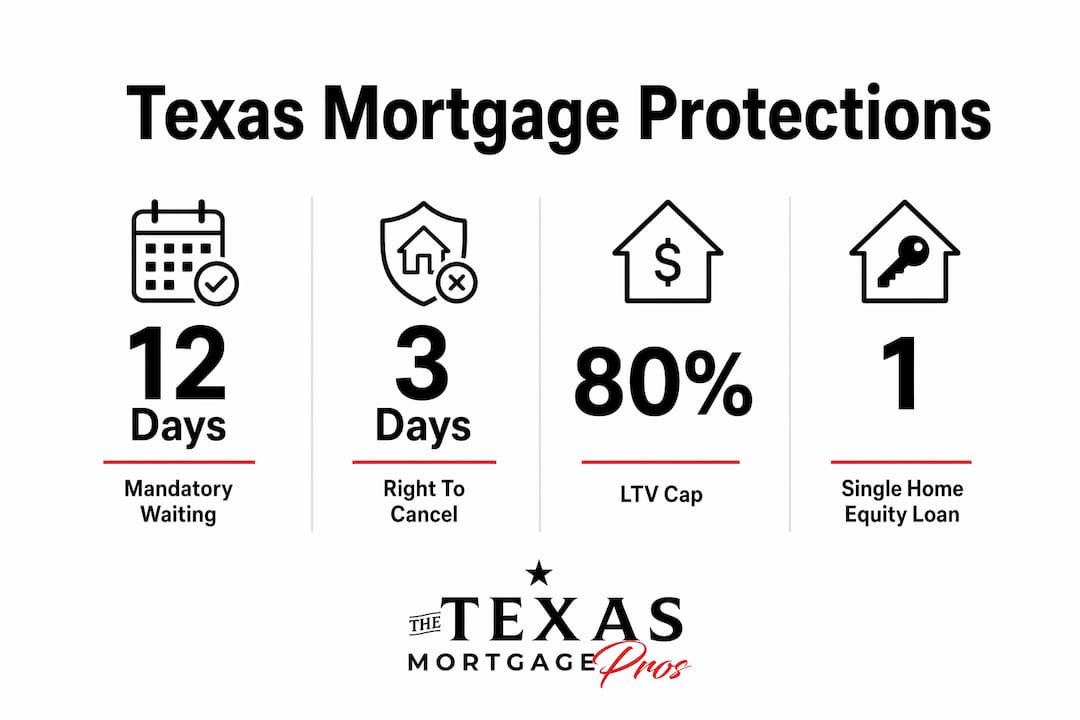

The most discussed protection is the 80% combined loan-to-value cap. A homeowner cannot borrow against their home if doing so would push all outstanding mortgage debt above 80% of the property’s appraised value. This rule guarantees that every Texas homeowner retains at least 20% equity at all times. That single requirement separates Texas from nearly every other state.

Beyond the LTV cap, Texas law imposes a detailed set of procedural and financial protections:

- In-person closing requirement: Borrowers must close at the office of a lender, licensed attorney, or title company. Remote or mail-away closings are not permitted for home equity loans.

- 12-day waiting period: Lenders must provide loan documents at least 12 days before closing. Borrowers have time to review terms without pressure.

- Three-day cancellation right: After closing, borrowers have 3 business days to cancel the loan without penalty.

- One loan at a time: Only one home equity loan or HELOC under Section 50(a)(6) can exist on a property at any time. Stacking is prohibited.

- 12-month seasoning rule: Owners must wait 12 months after closing a home equity product before obtaining another on the same property.

- HELOC minimum draw: Each HELOC draw must be at least $4,000. Credit cards, debit cards, and preprinted checks cannot be used to access HELOC funds.

- Fee cap: Lenders may charge no more than 2% of the loan principal in fees, excluding bona fide third-party costs. This cap limits the cost erosion of home equity at closing.

Pro Tip: If you are comparing home equity products, confirm that the lender’s fee estimate excludes third-party costs before accepting the 2% figure as the ceiling. Some lenders bundle costs in ways that obscure the total fee.

How do Texas mortgage laws prevent risks seen in other states?

Texas was the last state to legalize home equity lending, and it did so with strong consumer protections specifically designed to prevent the abuses that had emerged elsewhere. That caution proved prescient.

The 2008 housing crisis exposed what happens when homeowners can borrow against 95% or even 100% of their home’s value. When prices fell, millions of homeowners across the country owed more than their homes were worth. Texas homeowners largely avoided that outcome. The 80% LTV cap meant that even after a significant price decline, most Texas homeowners retained positive equity.

Texas mortgage laws shielded homeowners from the worst parts of the 2008 crisis. States without an 80% LTV cap saw widespread negative equity and foreclosure waves. Texas homeowners avoided large-scale foreclosure problems because the constitutional cap kept debt levels below the danger threshold.

The mandatory 12-day waiting period and the three-day cancellation right serve a different but related purpose. They prevent the high-pressure, same-day closings that characterized predatory lending in other markets. Borrowers have time to read documents, consult an attorney, and walk away if the terms do not fit.

Lender penalties reinforce every one of these protections. If a lender fails to cure a constitutional violation, it risks forfeiture of all principal and interest on the loan. That penalty is extraordinary by any standard. It creates a compliance culture among Texas lenders that goes well beyond what statutory penalties in other states typically produce.

What are the practical implications for borrowers and lenders in Texas?

Understanding the rules matters. Navigating them in practice is a different skill. Both borrowers and lenders face specific operational requirements that do not exist in most other states.

For lenders, the compliance burden starts with documentation. Texas lenders must use state-specific “Texas Home Equity Uniform Instruments.” Generic national forms are invalid and represent one of the most common fatal errors in Texas home equity lending. A national lender rolling out a HELOC product designed for other states must revise every form, every disclosure, and every closing procedure before offering it in Texas.

Texas law also requires that any instrument affecting real property title be prepared or reviewed by a Texas-licensed attorney. That requirement adds cost and time to every transaction, but it also reduces the risk of defective documents that could void the lien.

For borrowers, the practical implications are equally concrete. Here is what to expect when pursuing a home equity loan or HELOC in Texas:

- Budget for a longer timeline. The 12-day waiting period alone adds nearly two weeks to the process. Factor that into any financial planning that depends on a specific closing date.

- Confirm your equity position before applying. Calculate your combined LTV before submitting an application. If your current mortgage balance plus the requested loan amount exceeds 80% of your home’s appraised value, the loan will not close.

- Plan around the one-loan rule. If you already have a home equity loan or HELOC open, you cannot open another until the first is paid off. Structure your borrowing needs accordingly.

- Arrange in-person closing logistics early. Identify a lender’s office, attorney, or title company near you before you need one. Remote closing is not an option for these products.

- Understand HELOC draw limits. Each draw must be at least $4,000, and you cannot use a card or check to access funds. Plan draws in advance rather than treating the line like a checking account.

Pro Tip: Work with a lender who specializes in Texas home equity products. National lenders sometimes misquote timelines or offer non-compliant products because their standard processes were built for other states. A Texas-focused lender knows these rules by default.

Borrowers who want to review Texas home equity loan rules in full detail before applying will find that preparation significantly reduces surprises at closing.

Key Takeaways

Texas mortgage law is constitutionally embedded, making its homeowner protections among the most stable and strict in the United States.

| Point | Details |

|---|---|

| Constitutional foundation | Article XVI, Section 50(a)(6) governs all Texas home equity lending; changes require a statewide vote. |

| 80% LTV cap | Borrowers cannot exceed an 80% combined loan-to-value ratio, ensuring at least 20% equity at all times. |

| Mandatory waiting periods | A 12-day pre-closing window and a three-day post-closing cancellation right protect borrowers from rushed decisions. |

| One loan at a time | Texas prohibits stacking home equity loans; only one Section 50(a)(6) product per property at any time. |

| Lender penalty risk | Non-compliant lenders risk forfeiting all principal and interest, driving strict adherence across the market. |

Texas mortgage laws reward patience, but they demand preparation

I have spent years watching homebuyers and real estate professionals react with surprise when they first encounter Texas home equity rules. The 12-day waiting period frustrates people who expect a fast close. The in-person closing requirement catches remote buyers off guard. The one-loan rule derails financing strategies that would work perfectly in any other state.

My honest view is that the frustration is worth it. The constitutional structure of Texas mortgage law is not an instance of bureaucratic overreach. It is the reason Texas homeowners came through 2008 with their equity largely intact while homeowners in other states lost everything. The 80% LTV cap is not a restriction. It is a floor that keeps you solvent when the market turns.

The challenge I see most often is not the rules themselves. It is borrowers and lenders who treat Texas like every other state. National lenders sometimes bring non-compliant forms. Borrowers sometimes plan closings without accounting for the waiting period. Both mistakes are avoidable with the right preparation. Real estate professionals who understand these rules become genuinely valuable to their clients, not just as agents but as guides through a process that has real legal teeth. If you are working in Texas real estate in 2026, knowing these laws is not optional. It is the baseline.

— Michelle

How The Texas Mortgage Pros can help you navigate Texas mortgage rules

Texas mortgage regulations require lenders and borrowers to know the rules before the process starts. The Texas Mortgage Pros works with a network of over 70 lenders, all experienced with Texas constitutional mortgage requirements. That means compliant forms, accurate timelines, and loan products built specifically for Texas borrowers.

Whether you are a first-time buyer trying to understand your borrowing limits or a real estate professional advising a client on a home equity strategy, The Texas Mortgage Pros offers the guidance you need. Use the mortgage payment calculator to estimate your numbers before you apply, or explore specialty loan programs designed for Texas borrowers who need options beyond conventional products. The Texas Mortgage Pros is ready to help you close with confidence.

FAQ

Why did Texas legalize home equity lending so late?

Texas legalized home equity lending in 1998, the last state to do so, because lawmakers wanted strong constitutional protections in place before permitting it. The delay reflected a deliberate effort to prevent the predatory lending practices that had emerged in other states.

What is the 80% LTV rule in Texas?

The 80% combined loan-to-value rule caps total mortgage debt at 80% of the home’s appraised value. This constitutional limit guarantees that Texas homeowners retain at least 20% equity after any home equity borrowing.

Can I have two home equity loans in Texas at the same time?

No. Texas law allows only one home equity loan or HELOC under Section 50(a)(6) on a property at any time. Borrowers must also wait 12 months after closing one product before opening another on the same property.

What happens if a lender violates Texas home equity rules?

A lender that fails to cure a constitutional violation risks forfeiting all principal and interest on the loan. This penalty is among the harshest in any state and drives strict compliance across the Texas mortgage market.

Do Texas home equity rules apply to investment properties?

No. Section 50(a)(6) protections apply only to a borrower’s primary residence. Investment properties and second homes are not covered by the constitutional home equity lending rules.