A Texas new construction loan is a short-term financing product that funds the building of a new home through staged disbursements tied directly to construction milestones. Unlike a standard mortgage, which pays for a property that already exists, this type of loan finances something that has not been built yet. That distinction changes everything about how lenders qualify you, how funds are released, and what you pay during the build. Whether you are a first-time buyer or someone building a custom home, understanding how these loans work before you break ground saves you time, money, and real stress.

What is a Texas new construction loan and how does it work?

A Texas new construction loan is a specialized short-term credit facility, typically lasting 12 to 24 months, that covers the cost of building a home from the ground up. The industry term most lenders use is a “construction loan” or “construction-to-permanent loan,” depending on the structure you choose. Both terms describe the same core concept: a lender advances money in stages as your home gets built, rather than handing over a lump sum at closing.

The fundamental difference between a construction loan and a standard mortgage is that the lender is financing a property that does not yet exist. That raises the lender’s risk considerably, which is why the qualification process is more rigorous and the interest rates tend to run higher. You are not just proving you can repay a loan. You are also proving that the project itself will be completed successfully.

During the build, you make interest-only payments on the amount actually drawn, not the full loan balance. If your total loan is $400,000 but only $150,000 has been disbursed so far, you pay interest on $150,000. That structure keeps your monthly carrying costs manageable while construction is underway. Once the home is complete, the loan either converts to a permanent mortgage or gets paid off through a separate refinance.

How do construction loan draw schedules and payments work?

Funds are disbursed in stages tied to verified construction milestones. Common draw points include foundation completion, framing, rough-in work for plumbing and electrical, drywall installation, and final completion. Before each draw is released, the lender typically sends an inspector to confirm that the work described has actually been done. This protects both you and the lender from funds being misused or construction falling behind.

Here is a typical draw sequence for a Texas new construction project:

- Land and site preparation — Initial draw covers lot clearing, grading, and utility connections.

- Foundation — Funds released after the concrete slab or pier-and-beam foundation passes inspection.

- Framing — Walls, roof structure, and exterior sheathing trigger the next disbursement.

- Rough-in systems — Plumbing, electrical, and HVAC rough-in work verified before release.

- Drywall and interior — Interior finishes, insulation, and drywall completion unlock the next draw.

- Final completion — Certificate of occupancy and punch-list sign-off release the last funds.

Pro Tip: Ask your lender for the full draw schedule in writing before you sign anything. Knowing exactly when funds are released helps you and your builder plan the construction timeline without cash-flow gaps.

Because you pay interest only on amounts drawn, your monthly payment increases as construction progresses. Budget for this increase so it does not catch you off guard in the final months of the build.

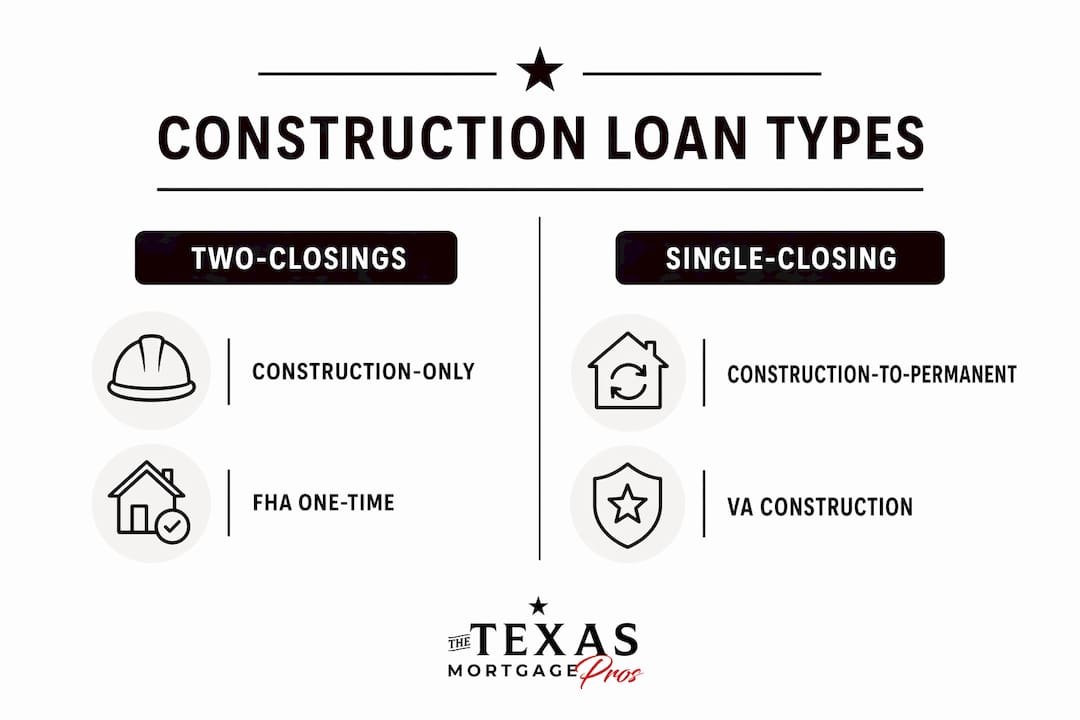

What types of construction loans are available to Texas homebuyers?

Texas homebuyers have four main loan structures to consider, each with different cost profiles and qualification requirements.

| Loan Type | Closings | Down Payment | Best For |

|---|---|---|---|

| Construction-only loan | Two (construction + permanent) | 20%–30% typical | Buyers who want flexibility at the permanent financing stage |

| Construction-to-permanent | One | 20%–30% typical | Buyers who want simplicity and rate certainty |

| FHA One-Time Close | One | As low as 3.5% | First-time buyers with lower credit or savings |

| VA construction loan | One | 0% for eligible veterans | Active military and veterans building in Texas |

Construction-only loans require two separate closings, meaning two sets of closing costs. You close on the construction loan first, then refinance into a permanent mortgage once the home is complete. Two closings add cost and complexity, but they give you the freedom to shop for the best permanent mortgage rate after construction ends.

Construction-to-permanent loans combine both phases into a single closing. You lock your rate at the start, which protects you if rates rise during the build. One-time-close loans eliminate duplicate closing costs and significantly reduce paperwork. For most first-time buyers in Texas, this structure is the cleaner path.

FHA One-Time Close loans open the door for buyers who cannot meet the 20% down payment threshold. FHA construction loans carry mortgage insurance premiums and loan limits, so they are not ideal for high-end custom builds. However, they are a practical option for buyers building a modest primary residence. You can learn more about FHA loan eligibility to see if this path fits your situation.

VA construction loans allow eligible veterans and active-duty service members to build with zero down payment. The VA program requires that the builder be VA-approved and that the property meet VA minimum property standards. For veterans in Texas, this is one of the most powerful home-building loan options available. The VA loan Texas guide covers the full picture of eligibility.

What are the requirements for a Texas construction loan?

Lenders evaluate construction loan applications more carefully than standard purchase mortgages because the collateral does not yet exist. Meeting these requirements before you apply puts you in a much stronger position.

- Credit score: A score of 680 or higher improves your approval odds and secures better pricing on conventional construction loans. FHA and VA programs can accommodate lower scores, but expect stricter scrutiny on other factors.

- Down payment: Conventional loans typically require 20% to 30% down. FHA loans go as low as 3.5%, and VA loans offer 0% for qualified veterans.

- Builder qualifications: Your builder must be licensed, insured, and acceptable to the lender. Many lenders maintain an approved builder list. Working with a builder who has an existing relationship with lenders speeds up the approval process considerably.

- Detailed construction plans: Lenders require architectural drawings, specifications, and a signed construction contract before approving the loan.

- Permits: Building permits must be obtained or in process before funds are disbursed.

- Itemized budget: A line-item budget covering all hard costs (materials, labor) and soft costs (permits, architect fees, inspections) is required. Lenders also require contingency reserves of 5% to 10% to cover cost overruns.

- Land ownership or acquisition: If you already own the lot, that equity can count toward your down payment. If you are purchasing land as part of the project, the lender will factor that into the total loan amount.

Pro Tip: Get your builder pre-approved by your lender before you finalize your construction contract. A builder who is already vetted by the lender removes one of the biggest friction points in the approval process.

What costs and fees should you expect with a Texas construction loan?

Understanding the full cost picture before you commit prevents budget surprises mid-build.

Interest rates on construction loans run 0.5 to 1.5 percentage points higher than rates on permanent mortgages. That premium reflects the lender’s added risk during the construction phase. Once the loan converts to a permanent mortgage, your rate adjusts to standard market pricing. You can check current Texas mortgage rates to get a realistic baseline for your budgeting.

Your monthly interest payments grow as more funds are drawn. Early in the project, when only the foundation draw has been released, your payment is relatively small. By the final months, when most of the loan balance is outstanding, your interest payment is at its peak. Plan your cash flow accordingly.

Here is a cost summary by loan type:

| Cost Item | Conventional | FHA | VA |

|---|---|---|---|

| Down payment | 20%–30% | 3.5% | 0% |

| Mortgage insurance | None | Required | Funding fee only |

| Closings | One or two | One | One |

| Rate premium during build | 0.5%–1.5% above permanent | 0.5%–1.5% above permanent | 0.5%–1.5% above permanent |

Closing costs for a construction loan follow the same general structure as a standard mortgage, covering origination fees, title insurance, appraisal, and recording fees. If you choose a two-close structure, you pay those costs twice. The ground-up construction loan process also includes inspection fees at each draw stage, which are typically paid by the borrower.

Budget a contingency reserve of at least 5% of your total construction cost. Material prices and labor costs in Texas can shift during a multi-month build, and lenders expect you to have that buffer in place before they approve your loan.

How to apply for and secure a new construction loan in Texas

Securing a construction loan requires more preparation than a standard mortgage application. Follow these steps to move through the process efficiently.

- Get your finances in order. Pull your credit report, pay down revolving debt, and document two years of income history. Lenders scrutinize debt-to-income ratios closely on construction loans.

- Select your lot and builder. Confirm the builder is licensed and willing to work within a lender-managed draw schedule. Working with an experienced builder who has navigated lender draw processes before significantly reduces friction.

- Choose your loan type. Decide between a construction-to-permanent loan and a two-close structure based on your rate outlook and financial flexibility. First-time buyers generally benefit most from the one-time close approach.

- Gather your documentation. Collect architectural plans, construction contract, itemized budget, permits, builder license, and proof of land ownership or purchase agreement.

- Submit your application. Apply with a lender who specializes in Texas construction loans. The construction loan options offered by specialized lenders often include programs not offered by standard retail banks.

- Manage the draw process. Stay in close communication with your builder and lender throughout construction. Delays in submitting draw requests slow down your builder’s cash flow and can push your completion date.

- Convert or refinance. At project completion, your loan either automatically converts to a permanent mortgage or you close on a new loan. If rates have dropped during construction, a two-close structure gives you the chance to capture a better rate at this stage.

Key takeaways

A Texas new construction loan funds a home that does not yet exist, which is why it requires more documentation, a qualified builder, and a staged disbursement process that standard mortgages do not.

| Point | Details |

|---|---|

| Loan structure | Construction loans disburse funds in stages, tied to verified milestones, rather than as a lump sum. |

| Payment during build | You pay interest only on the amount drawn, keeping monthly costs lower during construction. |

| Loan type choice | Construction-to-permanent loans reduce complexity by offering a single closing and an early rate lock. |

| Down payment range | Conventional loans require 20%–30% down; FHA allows 3.5%; VA allows 0% for veterans. |

| Rate premium | Construction loan rates run 0.5%–1.5% higher than permanent mortgage rates during the build phase. |

What I’ve learned about Texas construction loans after years in the field

The biggest mistake I see first-time buyers make is treating a construction loan like a standard mortgage application. They show up without a signed builder contract, architectural drawings, or a realistic budget. Then they are surprised when the lender asks for more documentation and the timeline slips by weeks.

The second mistake is underestimating the contingency reserve. Buyers hear “5% to 10%” and think that sounds like a lot of extra money to set aside. In practice, material costs and labor rates in Texas can shift meaningfully over the course of a 12-month build. That reserve is not padding. It is protection.

My honest advice: choose the construction-to-permanent structure if you are a first-time buyer. Yes, you lock your rate before the build starts, and yes, rates could theoretically drop. But the simplicity of one closing, one set of paperwork, and one lender relationship is worth more than the speculative upside of a two-close strategy. I have watched buyers get burned trying to time the market on their permanent mortgage rate while managing an active construction project. It adds stress you do not need.

Finally, do not skip the first-time homebuyer programs available in Texas. Some of them layer on top of construction financing and can reduce your out-of-pocket costs at closing. Most buyers never ask about them because they assume they only apply to existing homes. That assumption costs real money.

Build your new home with the right financing partner

If you are ready to move from planning to building, The Texas Mortgage Pros works with a network of over 70 lenders to find the construction loan structure that fits your budget and timeline. Whether you are comparing FHA, VA, or conventional options, we walk you through every step from pre-qualification to the final draw.

Use our mortgage payment calculator to estimate your interest-only payments during construction and plan your monthly budget before you commit. When you are ready for a personalized rate quote, visit The Texas Mortgage Pros and connect with a loan specialist who knows Texas construction financing inside and out. We are here to help you build with confidence.

FAQ

What is a Texas new construction loan?

A Texas new construction loan is a short-term loan that finances the building of a new home through staged fund disbursements tied to construction milestones. It differs from a standard mortgage because it funds a property that does not yet exist.

How long does a Texas construction loan last?

Most Texas construction loans have terms of 12 to 24 months, covering the active building period. Upon completion, the loan either converts to a permanent mortgage or is paid off through refinancing.

What credit score do I need for a Texas construction loan?

A credit score of 680 or higher is the typical threshold for conventional construction loans in Texas. FHA and VA programs can accommodate lower scores, though other qualification factors are given closer scrutiny.

Can first-time buyers use a construction loan in Texas?

Yes. First-time buyers can use FHA One-Time Close construction loans with as little as 3.5% down, or VA construction loans with zero down if they qualify. Construction-to-permanent loans are often the most practical structure for first-time buyers.

What is the difference between a construction loan and a construction-to-permanent loan?

A construction-only loan requires two separate closings and two sets of closing costs. A construction-to-permanent loan combines both phases into a single closing, locks in your rate at the start, and simplifies the overall process.