An LLC, or limited liability company, is the most widely used legal structure for holding investment real estate because it separates your personal assets from the debts and lawsuits tied to a property. Real estate investors use an LLC for mortgage financing to create a legal barrier between their personal wealth and any liability that arises from the investment. This structure changes how lenders evaluate your loan, which loan products you qualify for, and how your taxes flow. Understanding these trade-offs is the first step toward building a portfolio that protects what you have already earned.

Why investors use an LLC for mortgage and asset protection

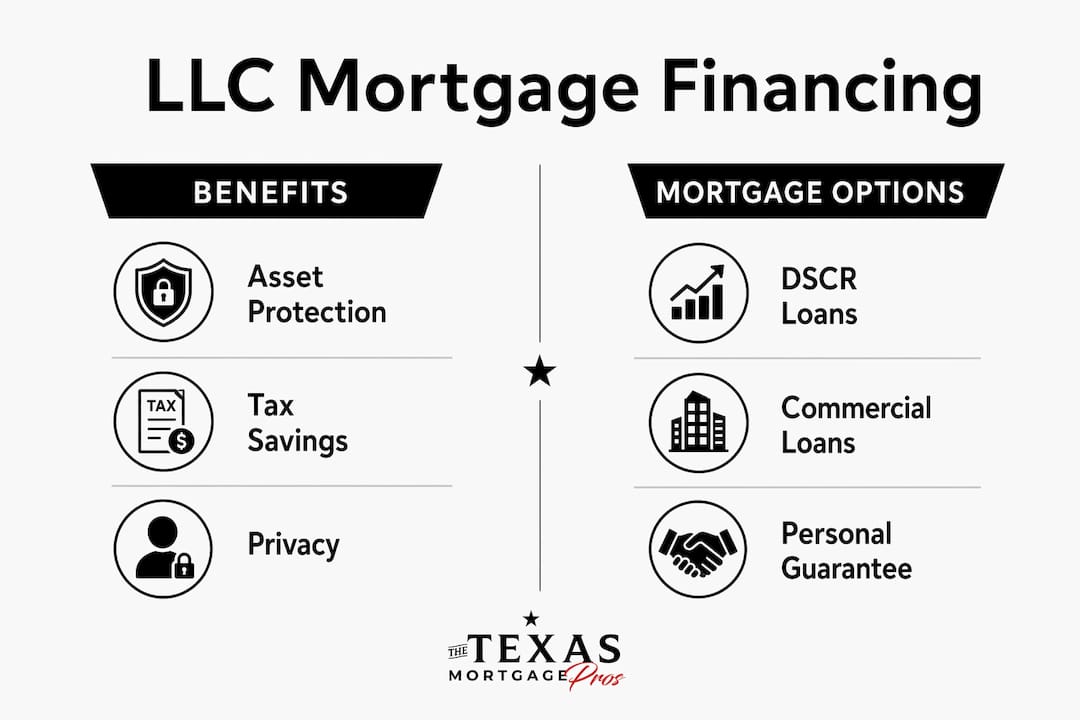

An LLC is a separate legal entity. That means the investment property, its mortgage, and any lawsuits connected to it belong to the LLC, not to you personally. If a tenant sues over an injury or a contractor files a lien, your personal bank accounts, home, and savings generally stay out of reach.

The protection works in both directions. Your personal credit problems do not automatically threaten the LLC’s property, and the property’s liabilities do not automatically threaten your personal finances. This legal separation of assets is the primary reason serious investors form LLCs before closing on a rental property.

That said, the shield has real limits. Most lenders require a personal guarantee on LLC mortgages, which means you are personally on the hook for the loan even if the LLC holds title. The guarantee does not erase liability protection for other claims, such as tenant lawsuits, but it does mean the lender can pursue you personally if the LLC defaults.

The other major risk is “piercing the corporate veil.” Courts can strip away LLC protection if you commingle personal and LLC finances. Paying personal bills from the LLC’s account, skipping annual reports, or signing contracts in your own name instead of the LLC’s name all give a court grounds to treat the LLC as if it never existed.

- Keep a dedicated LLC bank account and never mix personal funds with it.

- Sign all leases, contracts, and vendor agreements in the LLC’s name.

- File annual reports on time in your state to keep the entity in good standing.

- Hold formal meetings and document decisions, even if you are the sole member.

Pro Tip: Set up automatic reminders for your state’s annual report deadline. A missed filing can result in administrative dissolution, which wipes out your liability protection without any warning.

What mortgage options are available for LLC-owned properties?

Conventional loans backed by Fannie Mae or Freddie Mac are not available to LLCs. FHA and VA loans are also off the table. These programs require the borrower to be an individual, which means LLC investors must use a different category of loan products entirely.

The most common option is the DSCR loan, or Debt Service Coverage Ratio loan. A DSCR loan qualifies the property based on its rental income relative to the mortgage payment, not on your personal income. This makes it ideal for investors who own multiple properties or who are self-employed. DSCR loans are specifically designed for LLCs and investment properties, which is why they have become the default financing tool for this structure.

The cost difference is real. LLC mortgage rates run 0.5% to 3% higher than individual mortgage rates, and down payments typically fall in the 20%–30% range. That premium reflects the lender’s perception of higher risk when lending to an entity rather than a person.

Other financing options for LLC-owned properties include:

- Portfolio loans: Held by the lender rather than sold to the secondary market, giving more flexibility on underwriting criteria.

- Commercial loans: Used for larger or multi-unit properties, with shorter terms and balloon payments.

- Hard money loans: Short-term, asset-based financing used for fix-and-flip projects or bridge situations.

One strategy investors sometimes use is to buy a property in their personal names to access conventional rates, then transfer title to an LLC after closing. This approach carries serious risk. Most mortgages contain a due-on-sale clause that allows the lender to demand full repayment the moment title transfers. The “buy-and-quitclaim” method is often more expensive than financing an LLC directly from the start.

| Loan type | Available to LLCs | Key trade-off |

|---|---|---|

| Conventional (Fannie/Freddie) | No | Not accessible to entities |

| FHA / VA | No | Requires an individual borrower |

| DSCR loan | Yes | Higher rate, 20%–30% down |

| Portfolio loan | Yes | Flexible terms, lender-held |

| Hard money loan | Yes | Short-term, high-cost |

What are the tax and operational benefits of investing through an LLC?

Pass-through taxation is the default tax treatment for an LLC. Profits and losses flow directly to your personal tax return, so the entity itself pays no federal income tax. You can also elect S-Corp or C-Corp status if a different tax structure better fits your situation. That flexibility is uncommon in other business structures.

Privacy is another underrated benefit. When an LLC holds title, public property records show the LLC name, not yours. For investors who own multiple properties, this limits public exposure of their full portfolio.

Transferring ownership is also simpler with an LLC. Instead of recording a new deed, you can transfer membership interests in the LLC. This can reduce transfer taxes and simplify estate planning.

The operational costs are real, though. State LLC formation fees range from under $50 to over $500, with annual fees in some states reaching $800. If you hold each property in a separate LLC, those costs multiply with every acquisition. You also need separate bank accounts, bookkeeping, and registered agents for each entity.

The “one LLC per property” model limits cross-property liability. If a lawsuit targets one property, the others remain protected. The trade-off is administrative complexity. Investors with large portfolios often work with a real estate attorney and a CPA to decide whether a series LLC, a holding company structure, or individual LLCs make the most sense for their situation. For guidance on structuring real estate entities, business real estate consulting can help clarify which approach fits your portfolio size and risk tolerance.

What practical steps can help investors successfully finance LLC-owned properties?

Getting the structure right before you close is far easier than fixing it afterward. These steps reflect what experienced investors do to avoid the most common and costly mistakes.

- Form the LLC before you make an offer. Financing directly into the LLC from day one entirely avoids due-on-sale clause risk. Most DSCR lenders accept applications for a “to-be-formed” LLC, so you can start the loan process before the entity is officially registered.

- Choose the right loan type early. DSCR loans are the most practical option for most LLC investors. Confirm with your lender that the loan is structured for entity borrowers before you get deep into underwriting.

- Open a dedicated LLC bank account immediately. All rental income, mortgage payments, and property expenses must flow through this account. Mixing funds is the fastest way to lose your liability protection.

- Prepare your documentation. Lenders typically require the LLC’s Articles of Formation, an Employer Identification Number (EIN), and financial proof for the personal guarantor. Having these ready before you apply significantly shortens the timeline.

- Keep the LLC in good standing. Missed state filings can trigger administrative dissolution, which ends your liability protection and can complicate your mortgage. File annual reports on time and pay state fees without exception.

- Work with a real estate attorney and a mortgage professional. The legal and financing decisions interact in ways that are easy to get wrong. A qualified mortgage broker who works with investor clients can match you with lenders who specialize in LLC structures.

Pro Tip: Ask your mortgage broker specifically whether they work with DSCR lenders who accept LLC borrowers. Not every lender does, and working with one who does not will cost you time and money.

Investors who want to explore investment property loan options in Texas will find that lenders with experience in LLC financing handle the documentation and underwriting process more efficiently than general mortgage lenders.

Key Takeaways

Using an LLC for mortgage financing protects personal assets from property-related liabilities, but requires specialized loan products, higher costs, and disciplined entity maintenance to preserve that protection.

| Point | Details |

|---|---|

| Asset protection is conditional | LLC liability protection only holds if you maintain strict separation between personal and LLC finances. |

| Conventional loans are unavailable. | LLCs must use DSCR, portfolio, or commercial loans, which carry rates 0.5%–3% above individual mortgage rates. |

| Personal guarantees are standard. | Most lenders require personal guarantees on LLC mortgages, so personal liability for the loan remains. |

| Tax flexibility is a real advantage. | Pass-through taxation and optional S-Corp or C-Corp elections provide investors with meaningful tax-planning options. |

| Form the LLC before closing. | Financing directly into the LLC from the start avoids due-on-sale clause risk and simplifies the title chain. |

Why I think most investors underestimate the maintenance side of LLC ownership

After years of working with real estate investors, the pattern I see most often is this: investors spend months researching the right LLC structure, then neglect the ongoing maintenance that makes the structure actually work. They open the LLC, close on the property, and then start paying property expenses from a personal account because it is more convenient. That single habit can unravel everything they set up.

The liability protection an LLC provides is not automatic or permanent. Courts look at how you actually operate the entity, not just how it was formed. I have seen investors lose their protection in disputes not because their LLC was poorly structured, but because they could not demonstrate genuine separation in their financial records.

My honest advice to investors just starting: I recommend not forming an LLC for your first property unless you are ready to maintain it properly. A well-maintained LLC on your second or third property is far more valuable than a neglected one on your first. Scale into the structure as your portfolio and your administrative discipline grow together.

The other thing I would add is that an LLC alone is not a complete defense. Complementary insurance coverage is critical to a comprehensive asset protection plan. An umbrella policy and a landlord policy working alongside your LLC structure give you layers of protection that no single tool can provide on its own.

— Michelle

How The Texas Mortgage Pros supports LLC investors in Texas

Real estate investors using LLCs need lenders who understand entity-based financing, not lenders who treat every application like a standard home purchase. The Texas Mortgage Pros works with a network of over 70 lenders, including specialists in DSCR loans and non-qualified mortgage products designed for LLC-held investment properties.

Use the mortgage calculators to model your numbers before you apply, including estimated rates for LLC financing. When you are ready to move forward, The Texas Mortgage Pros can match you with lenders who work with LLC borrowers, guide you through the documentation requirements, and help you secure competitive rates on your investment property. Get your free mortgage quote and see what your LLC financing options look like today.

FAQ

Why do investors use an LLC for mortgage financing?

Investors use an LLC for mortgage financing to separate personal assets from property-related liabilities, including lawsuits and debts. The LLC holds title to the property, so personal wealth is generally protected from claims against the investment.

Can an LLC get a conventional mortgage?

No. Conventional loans backed by Fannie Mae or Freddie Mac require an individual borrower. LLCs typically finance properties with DSCR, portfolio, or commercial loans, which carry higher rates and larger down payment requirements.

What is a DSCR loan and why is it used for LLCs?

A DSCR loan qualifies the property based on rental income relative to the mortgage payment, not the borrower’s personal income. It is the most common mortgage product for LLC-owned investment properties because it is specifically designed for entity borrowers.

Does forming an LLC eliminate personal liability on the mortgage?

No. Most lenders require a personal guarantee on LLC mortgages, which means you remain personally liable for the loan. The LLC protects against other claims, such as tenant lawsuits, but the personal guarantee keeps you personally responsible for the debt.

What happens if I transfer a property to an LLC after closing?

Transferring title after closing can trigger the due-on-sale clause in your mortgage, allowing the lender to demand full repayment immediately. Financing directly into the LLC from the start is the safer approach and avoids this risk entirely.

Recommended

- Mortgage Calculators – The Texas Mortgage Pros

- Non-Qualified Mortgage Loans: Home Loan Programs for the Self-Employed – The Texas Mortgage Pros

- Streamlining Your Investments: The Role Of Loan Specialists In Investment Property Mortgages – The Texas Mortgage Pros

- Investment Property Loans & Mortgage Rates in Texas