A Non-QM loan is defined as any residential mortgage that does not meet the Consumer Financial Protection Bureau’s Qualified Mortgage standards, which cap debt-to-income ratios and restrict specific loan features. The industry term is “non-qualified mortgage,” and it opens the door for self-employed borrowers, real estate investors, and high-net-worth individuals who cannot satisfy standard W-2 or tax return requirements. These loans are not subprime products. They are carefully structured financing options for creditworthy borrowers whose income simply does not fit a conventional mold. If you have been told “no” by a traditional lender, non-QM explained in full may change your outlook entirely.

What makes non-qm different from a qualified mortgage?

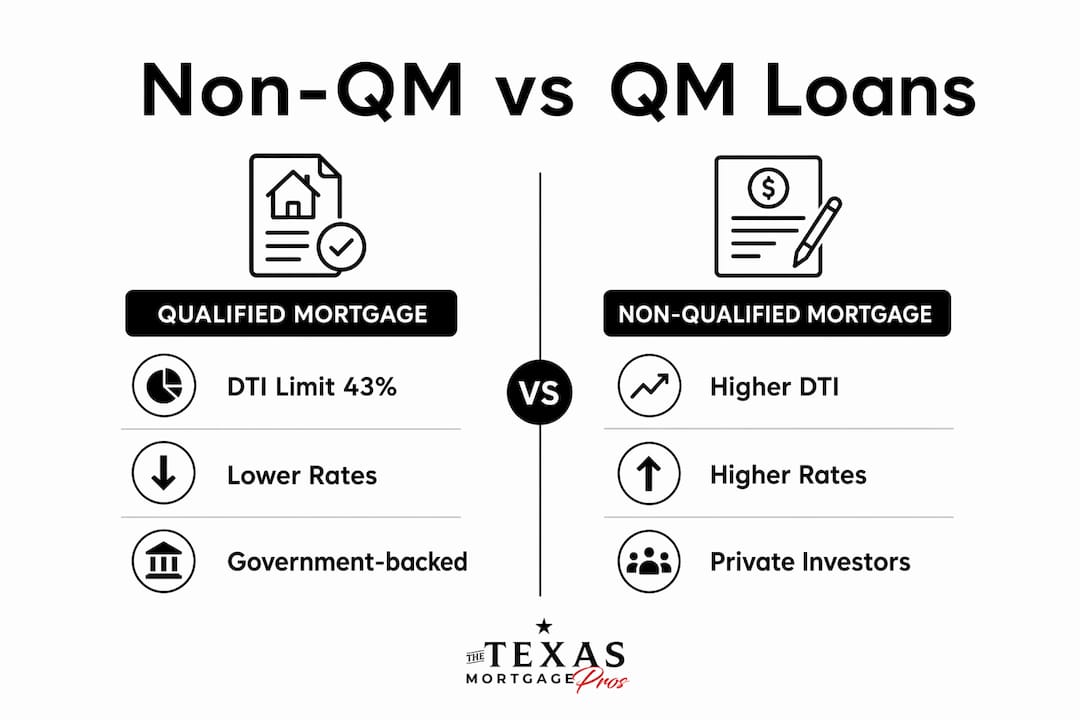

The CFPB’s Qualified Mortgage rule sets firm boundaries on what lenders can offer. Conventional QM loans cap the borrower’s debt-to-income ratio at 43%, require full income documentation such as W-2s and tax returns, and prohibit features like interest-only payments or balloon payments. Non-QM loans bypass these restrictions through alternative documentation and more flexible underwriting criteria.

The most significant structural difference is who holds the risk. Because Non-QM loans are not sold to government-sponsored enterprises like Fannie Mae or Freddie Mac, lenders keep them in their own portfolios or sell them to private investors. That retained risk is why Non-QM rates run higher than conventional rates. The lender is carrying more exposure, and the pricing reflects that reality.

Pro Tip: Ask any Non-QM lender upfront whether they portfolio the loan or sell it to a private investor. Portfolio lenders often have more flexibility on terms and may be more willing to work through unusual documentation scenarios.

Here is a direct comparison of the two loan categories:

| Criteria | Qualified Mortgage (QM) | Non-Qualified Mortgage (Non-QM) |

|---|---|---|

| DTI Limit | 43% maximum | Can exceed 50% in some programs |

| Income Documentation | W-2s and tax returns required | Bank statements, P&L, asset statements accepted |

| Government Backing | Fannie Mae or Freddie Mac eligible | No government backing; portfolio or private sale |

| Loan Features | No interest-only or balloon payments | Interest-only options available |

| Underwriting | Automated approval systems | Manual review process |

| Borrower Profile | Salaried employees, standard credit | Self-employed, investors, complex income |

The table above shows that Non-QM is not a lesser product. It is a different product built for a different borrower profile.

What are the main non-qm loan types?

Common Non-QM loan types include DSCR, Bank Statement, Profit and Loss, and Asset Depletion loans. Each one uses a different method to verify that you can repay the loan without relying on traditional employment records. Understanding which type fits your situation is the first step toward a successful application.

- DSCR Loans (Debt Service Coverage Ratio): These loans qualify real estate investors based on the rental income a property generates, not the borrower’s personal income. If the property’s monthly rent covers the mortgage payment, you can qualify. This is the go-to option for investors building a rental portfolio in Texas.

- Bank Statement Loans: Designed for self-employed borrowers, these programs use 12 or 24 months of personal or business bank deposits to calculate income. You do not need to provide tax returns. This matters because many self-employed individuals write off significant expenses, which lowers their taxable income and disqualifies them from conventional loans even when their cash flow is strong.

- Profit and Loss Statement Loans: A CPA-prepared P&L statement replaces tax returns as the income document. This option works well for business owners who want a current snapshot of earnings rather than a two-year average from prior tax filings.

- Asset Depletion Loans: High-net-worth borrowers with substantial liquid assets but limited monthly income can qualify by dividing their total assets over a set number of months to create a calculated monthly income figure. A borrower with $2 million in a brokerage account, for example, may qualify even without a paycheck.

Alternative income documentation options also include rental income statements and asset account summaries, giving lenders multiple ways to assess repayment ability. The common thread across all types is that none of them require W-2s or standard tax returns.

Pro Tip: If you are self-employed, compare the Bank Statement loan option against the P&L option with your CPA before applying. The income figure each method produces can differ significantly, and the higher number directly affects your loan amount.

You can explore self-employed home loan options in more detail to see which documentation path fits your business structure.

What do non-qm loans cost and require?

Non-QM loans carry real financial trade-offs. Understanding them before you apply puts you in a stronger negotiating position and prevents surprises at closing.

Down payment requirements

Non-QM loans require higher down payments, typically between 15% and 30%. That range exceeds the median 10% down payment for first-time buyers on conventional loans. The larger down payment reduces lender risk and partially offsets the absence of government backing.

Interest rate expectations

Non-QM loans carry higher interest rates than conventional mortgages. The exact premium depends on your credit score, loan-to-value ratio, and the specific program you choose. Borrowers with strong credit and a 25% down payment will see better rates than those with thinner credit files and a minimum down payment.

Underwriting timeline

The underwriting process is more manual and takes longer than automated conventional approvals. Plan for a longer review period and gather your documentation early. Lenders will scrutinize bank statements, asset accounts, and rental income records carefully.

Here is a summary of typical Non-QM loan requirements:

| Requirement | Typical Non-QM Range | Conventional Comparison |

|---|---|---|

| Down Payment | 15%–30% | 3%–10% for most programs |

| Credit Score | 620–680 minimum (varies by lender) | 620 minimum for most QM loans |

| DTI Ratio | Up to 50%+ with compensating factors | 43% maximum |

| Loan Review | Manual underwriting | Automated system |

| Waiting Period After Bankruptcy | Some lenders offer no waiting period | 1–7 years depending on event |

The waiting period detail is worth noting. Some Non-QM lenders offer loans with no waiting period after a bankruptcy, while conventional loans require 1–7 years depending on the event type. For borrowers rebuilding after a financial setback, this flexibility can be the deciding factor.

Use a mortgage payment calculator to model the monthly cost difference between a Non-QM rate and a conventional rate before committing to a program.

Who should consider a non-qm loan?

Non-QM loans provide an alternative for self-employed borrowers, real estate investors, and high-net-worth individuals with nontraditional income streams. The right borrower for a Non-QM loan shares one common trait: their financial strength does not show up cleanly on a tax return or pay stub.

Consider a Non-QM loan if you fall into one of these situations:

- You are self-employed and your tax returns understate your income. Business deductions reduce taxable income, which can disqualify you from conventional loans even when your cash flow is healthy.

- You are a real estate investor qualifying on rental income. DSCR loans let the property’s income do the qualifying work, not your personal W-2.

- You experienced a recent credit event. Bankruptcy, foreclosure, or a short sale may not disqualify you from a Non-QM loan the way it would from a conventional product.

- You have significant assets but limited monthly income. Retirees and high-net-worth individuals often fit this profile. Asset Depletion loans convert liquid wealth into qualifying income.

- Your DTI ratio exceeds conventional limits. If your debt load pushes past 43%, Non-QM programs that allow DTI above 50% may still get you approved.

Conventional loans remain the better choice when you qualify for them. The lower rate and smaller down payment produce a lower total cost of borrowing. Non-QM is the right tool when conventional financing is genuinely out of reach, not simply inconvenient. Evaluate the rate difference carefully and calculate the long-term cost before deciding. The non-qualified mortgage programs available today are more varied than most borrowers realize, which means comparison shopping matters more than ever.

Key takeaways

Non-QM loans are the most practical financing path for creditworthy borrowers whose income, assets, or credit history does not meet CFPB Qualified Mortgage standards.

| Point | Details |

|---|---|

| Core Definition | Non-QM loans do not meet CFPB QM rules and use alternative income documentation instead of W-2s. |

| Higher Upfront Costs | Expect a down payment of 15%–30% and higher interest rates compared to conventional loans. |

| Four Main Loan Types | DSCR, Bank Statement, P&L, and Asset Depletion loans each qualify borrowers differently. |

| Not Subprime | Non-QM loans serve financially sound borrowers with complex income, not high-risk borrowers. |

| Best Fit Borrowers | Self-employed individuals, real estate investors, and those with recent credit events benefit most. |

Why non-qm gets a bad reputation it does not deserve

The assumption that Non-QM equals subprime is one of the most persistent and damaging myths in mortgage lending. Non-QM mortgages are not automatically subprime. They are often carefully underwritten loans for creditworthy individuals whose financial complexity simply does not fit a government-backed template.

I have seen this play out repeatedly. A business owner with $400,000 in annual deposits gets turned down by a conventional lender because their Schedule C shows $80,000 in taxable income after deductions. That borrower is not a credit risk. They are a documentation mismatch. A Bank Statement loan solves that problem cleanly.

The real caution with Non-QM is not the product itself. It is working with lenders who do not specialize in it. Non-QM underwriting is manual and judgment-based. An inexperienced lender will either deny a perfectly qualified borrower or approve someone who should not be borrowing at that level. Both outcomes are bad. Work with a lender who has a track record in the specific Non-QM program you need, not one who offers it as a side product.

The other thing I would push back on is the idea that Non-QM is always a last resort. For a real estate investor running five rental properties, a DSCR loan is often the first choice, not a fallback. It keeps personal income separate from investment qualification and scales cleanly as the portfolio grows. That is a strategic decision, not a sign of financial weakness.

— Michelle

How the texas mortgage pros can help you find the right loan

The Texas Mortgage Pros works with a network of over 70 lenders to match Texas borrowers with the right Non-QM program for their situation. Whether you are self-employed, investing in rental properties, or rebuilding after a credit event, we have access to DSCR, Bank Statement, P&L, and Asset Depletion programs that conventional lenders simply do not offer.

Our team guides you through every step, from gathering the right documentation to comparing loan terms across multiple lenders. We also offer mortgage calculators so you can model your monthly payment before you apply. For borrowers who need help with upfront costs, we can connect you with down payment assistance programs designed for Texas homebuyers. Explore our full range of specialty loan products and get pre-qualified today.

FAQ

What is a non-qm loan in simple terms?

A Non-QM loan is a mortgage that does not follow the CFPB’s Qualified Mortgage rules, allowing borrowers to qualify using bank statements, rental income, or assets instead of W-2s and tax returns.

Are non-qm loans riskier than conventional mortgages?

Non-QM loans carry higher costs for borrowers, including larger down payments and higher interest rates, but they are not inherently riskier when properly underwritten for creditworthy borrowers with complex income profiles.

What credit score do you need for a non-qm loan?

Most Non-QM lenders require a minimum credit score in the 620–680 range, though the exact threshold varies by lender and program type.

Can a self-employed borrower use a non-qm loan?

Yes. Bank Statement loans and P&L loans are specifically designed for self-employed borrowers who cannot document income through standard tax returns or W-2 forms.

How long does non-qm underwriting take?

Non-QM underwriting is a manual process and typically takes longer than automated conventional approvals, so borrowers should plan for additional review time and prepare documentation early.