Your mortgage term is the length of time your loan agreement locks in your interest rate and conditions before you must renew, refinance, or pay off the balance. Choosing the right mortgage term shapes your monthly payment, total interest cost, and financial flexibility for years to come. Most American homebuyers pick between 15, 20, and 30-year fixed-rate loans, though adjustable-rate options add more variables to the decision. The Texas Mortgage Pros works with over 70 lenders to help first-time buyers sort through these choices and find a term that fits their actual budget and goals, not just the most popular option.

How different mortgage term lengths affect your finances

The core tradeoff in selecting a mortgage duration is simple: shorter terms cost less overall but demand higher monthly payments, while longer terms lower your monthly obligation but increase total interest paid. Shorter terms carry lower rates but higher monthly payments, while 30-year loans spread costs out at a higher total interest expense. That difference in total interest can reach tens of thousands of dollars over the life of a loan.

Comparing the three most common term lengths

The table below shows how term length shifts your payment and total cost on a $300,000 loan at representative rates:

| Term | Approx. monthly payment | Total interest paid |

|---|---|---|

| 15-year | ~$2,100 | ~$78,000 |

| 20-year | ~$1,800 | ~$132,000 |

| 30-year | ~$1,450 | ~$222,000 |

Note: Figures are illustrative estimates based on approximate market rates. Actual payments vary by lender and credit profile.

The 20-year mortgage is a powerful compromise that most buyers overlook. 20-year loans often carry rates 0.10–0.25% lower than 30-year loans, with payments that fall between the 15 and 30-year options. That middle ground delivers real interest savings without the steep monthly commitment of a 15-year loan.

Equity builds faster on shorter terms because more of each payment goes toward principal from the start. On a 30-year loan, the first several years of payments are weighted heavily toward interest. A 15-year loan flips that ratio much sooner, building ownership stake at roughly twice the pace.

Pro Tip: If a 15-year payment feels tight, consider a 20-year term. You save significantly on interest compared to a 30-year loan while keeping your monthly payment more manageable.

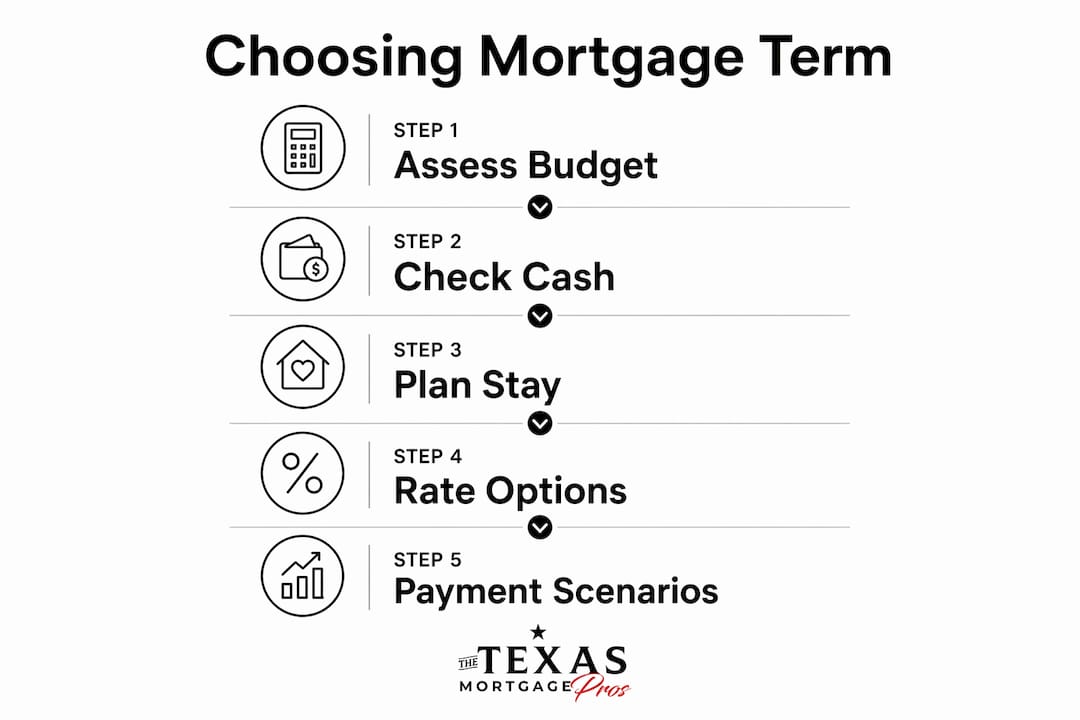

How to choose the right mortgage term step by step

No universally right mortgage term exists. The optimal choice balances income security and life plans to fit your risk tolerance. Here is a practical process to work through before you commit.

Step 1: Assess your monthly budget honestly

Start with your take-home pay, not your gross income. Add up your fixed expenses, including car payments, student loans, and insurance. The payment you can afford on paper and the payment that leaves you financially comfortable are often different numbers. Financial experts advise against choosing a term that jeopardizes your financial stability, even when a shorter term looks cheaper overall.

Step 2: Check your emergency fund and cash flow

A tight monthly payment with no cash reserve is a risk. If your income is variable or you are early in your career, a longer term gives you a lower required payment each month. Longer terms allow lower mandatory payments and more flexibility when income dips or unexpected expenses hit.

Step 3: Consider how long you plan to stay

This step catches many buyers off guard. If you expect to sell or relocate within seven years, a 30-year term may actually serve you better than a 15-year term, because your monthly savings give you more cash to work with. Breaking a mortgage term early can trigger prepayment penalties, which erodes any interest savings you planned on.

Step 4: Evaluate fixed vs. adjustable rate options

A fixed-rate mortgage locks your rate for the full term. An adjustable-rate mortgage (ARM) starts lower but resets after an initial period, typically 5, 7, or 10 years. Understanding how interest rates affect your total cost is critical before choosing between these structures. If you plan to sell before the ARM resets, the lower initial rate can save money. If you plan to stay long term, a fixed rate removes the risk of a future rate spike.

Step 5: Run multiple payment scenarios

Use a mortgage calculator before you speak with a lender. Input your loan amount, test different term lengths, and compare the monthly payment and total interest side by side. Seeing the numbers in front of you makes the tradeoff concrete rather than abstract.

Pro Tip: Choose a 30-year loan and make extra principal payments when cash flow allows. Overpaying on a 30-year loan can achieve interest savings similar to a 15-year loan while keeping your required payment lower for months when money is tight.

What mistakes should you avoid when selecting your mortgage term?

First-time buyers repeat the same errors. Knowing them in advance saves real money and stress.

- Overextending on monthly payments. Choosing a 15-year term because it looks cheaper overall is a mistake if the payment strains your budget every month. One job loss or medical bill can put you in a difficult position.

- Ignoring how soon you might move. Seven out of ten repeat homebuyers moved sooner than they planned, which exposed them to prepayment penalties. Be realistic about your timeline.

- Overlooking prepayment penalties. Some loan products charge fees for paying off or refinancing before the term ends. Read the fine print before signing.

- Discounting future income changes. A promotion, a career shift, or a growing family all affect what you can comfortably pay. Build in a margin for life changes.

- Locking in without comparing options. Many buyers accept the first term structure a lender offers. Reviewing types of mortgage loans before you commit gives you a clearer picture of what is available.

“Mortgage term choice represents a forecast about interest rates. Locking in longer terms buys certainty, but at a premium.” — Canada Mortgage Source

Lenders also impose age-based limits on term length. Borrowers aged 40 may be limited to 30–35 year terms due to lender policies that require repayment before age 70–75. That constraint narrows your options if you are buying later in life, so factor it into your planning early.

How to use mortgage calculators to compare your options

Mortgage calculators are the fastest way to calculate mortgage term length impacts without guessing. The right calculator lets you test multiple scenarios in minutes and see exactly how term length changes your financial picture.

Here is what to look for in a good mortgage calculator:

- Loan amount and interest rate inputs. Enter the actual loan amount you expect to borrow and the current rate you qualify for, not a generic estimate.

- Term length comparison. The best tools let you run a 15, 20, and 30-year scenario side by side so you can see payment and total interest differences at a glance.

- Extra payment modeling. Some calculators show how making one extra payment per year or adding $200 per month to principal shortens your effective payoff date.

- Fixed vs. adjustable rate toggle. If you are weighing adjustable rate mortgages against fixed options, a calculator that models both helps you see the rate-reset risk clearly.

The Texas Mortgage Pros offers mortgage calculators built specifically for Texas homebuyers. You can input your loan amount, test different term lengths, and compare total costs without committing to anything.

Pro Tip: Run your numbers at a rate that is 0.5% higher than your current quote. That stress test shows whether you can still afford the payment if rates shift before you close or if you refinance later.

Key takeaways

The best mortgage term is the one that keeps your monthly payment comfortable while minimizing total interest cost over the time you actually plan to stay in the home.

| Point | Details |

|---|---|

| Shorter terms cost less overall | A 15-year loan saves tens of thousands in interest but requires a higher monthly payment. |

| The 20-year term is underused | It delivers meaningful interest savings with payments more affordable than a 15-year loan. |

| Longer terms offer flexibility | A 30-year loan with extra payments can match a 15-year payoff while protecting cash flow. |

| Moving plans matter | Breaking a term early triggers penalties, so match your term to how long you plan to stay. |

| Calculators are non-negotiable | Run multiple term scenarios before you commit to see the real cost difference. |

What I have learned about picking a mortgage term

I have worked with enough first-time buyers to know that the 15-year mortgage gets oversold. It looks great on paper because the total interest savings are real and significant. But I have seen buyers stretch into a 15-year payment and then feel trapped every time an unexpected expense hits. That stress is not worth the savings if it means you have no financial cushion.

My honest recommendation for most first-time buyers is to start with a 30-year fixed-rate loan and treat extra payments as a habit rather than a requirement. You get the lower mandatory payment as a safety net, and you still build equity faster when your cash flow allows it. That combination gives you the best of both worlds without locking you into a payment that leaves no room to breathe.

The buyers I have seen make the best decisions are the ones who run their numbers honestly, factor in a realistic timeline for staying in the home, and ask their lender the right questions before signing. If you are unsure what to ask, a first-timer’s lender guide is a good place to start. The mortgage term you choose is not just a financial decision. It is a reflection of where you are in life and where you plan to go.

— Michelle

Find the right mortgage term with The Texas Mortgage Pros

Choosing the right loan structure is easier when you have the right tools and the right team behind you. The Texas Mortgage Pros gives Texas homebuyers access to interactive mortgage calculators that let you compare 15, 20, and 30-year scenarios side by side with real numbers. Our team works with over 70 lenders to find competitive rates that match your term preference and financial goals.

Whether you are exploring first-time homebuyer programs or trying to decide between a fixed and adjustable rate, we are here to guide you from your first question to closing day. Get pre-qualified today and let us help you find a mortgage term that works for your life, not just your loan.

FAQ

What is the most common mortgage term length?

The 30-year fixed-rate mortgage is the most common choice among American homebuyers because it offers the lowest required monthly payment. Shorter terms like 15 and 20 years are popular with buyers who want to pay less total interest and build equity faster.

Is a 15-year or 30-year mortgage better for first-time buyers?

A 30-year mortgage is often the better starting point for first-time buyers because the lower payment protects cash flow. Making extra principal payments on a 30-year loan can replicate the interest savings of a 15-year term without locking you into a higher required payment.

What happens if I break my mortgage term early?

Breaking a mortgage term before it ends typically triggers a prepayment penalty, which can cost thousands of dollars. Seven out of ten repeat homebuyers moved sooner than planned, so always check your loan’s prepayment terms before signing.

How does an adjustable-rate mortgage term differ from a fixed-rate term?

A fixed-rate mortgage locks your interest rate for the full loan term, giving you predictable payments. An adjustable-rate mortgage starts with a lower rate that resets after an initial period, which can increase your payment if rates rise.

Can I pay off my mortgage faster without refinancing?

Yes. Making extra principal payments on any mortgage term reduces your balance faster and cuts total interest paid. This strategy works especially well on a 30-year loan, where extra payments simulate the payoff speed of a shorter term while keeping your required monthly payment low.