Shorten mortgage term refinancing is defined as replacing your existing mortgage with a new loan that has a shorter repayment period, typically moving from a 30-year loan to a 15- or 20-year term. The industry standard term for this strategy is a rate-and-term refinance, which changes your interest rate, loan term, or both without cashing out equity. Refinancing to a shorter term builds equity faster and cuts total interest paid, though it usually raises your monthly payment. The Texas Mortgage Pros works with over 70 lenders to help Texas homeowners find the most competitive rates for this exact strategy. With approximately 2.7 million homeowners holding 30-year fixed mortgages that could benefit from refinancing by early 2026, the opportunity is real and worth evaluating carefully.

How do you know if shorten mortgage term refinancing is right for you?

The clearest signal that a shorter-term refinance makes sense is a meaningful gap between your current rate and today’s market rates. The mortgage industry rule of thumb says refinancing is worth pursuing when your rate drops by 0.75 to 1 percentage point. That gap creates enough monthly savings to offset closing costs within a reasonable timeframe.

Your homeownership timeline matters just as much as the rate gap. If you plan to sell or move within a few years, the upfront costs of refinancing may never pay off. The break-even point is calculated by dividing your total closing costs by your monthly savings. If that number is 36 months and you plan to stay for 10 years, refinancing makes strong financial sense.

Before you apply, review these key eligibility factors:

- Credit score: Most lenders require a score of 620 or higher for a conventional refinance, with better rates available above 740.

- Home equity: You generally need at least 20% equity to avoid private mortgage insurance on the new loan.

- Debt-to-income ratio: Lenders typically want your total monthly debt payments to stay below 43% of your gross income.

- Stable income: A consistent employment history of at least two years strengthens your application.

- Current loan balance: The remaining balance and term on your existing mortgage affect whether shortening the term is financially logical.

One factor homeowners often overlook is cash flow. Shortening the mortgage term through refinancing increases your monthly payment, so you must confirm the higher payment fits your budget without creating financial strain. A 15-year loan on a $280,000 balance will carry a noticeably higher monthly payment than the same balance spread over 30 years.

Pro Tip: Run your break-even calculation before you even call a lender. Divide your estimated closing costs by your projected monthly savings. If the result is longer than your planned time in the home, skip the refinance and consider extra principal payments instead.

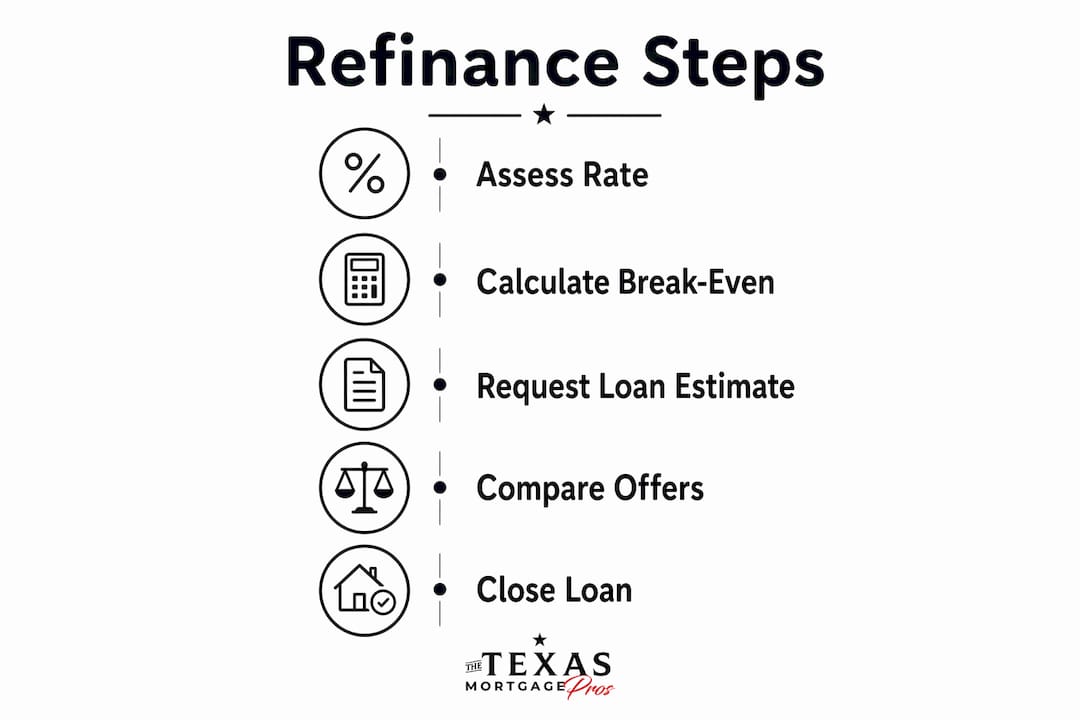

What are the steps to refinance your mortgage to a shorter term?

A shorter-term refinance follows a clear process. Moving through each step carefully prevents costly surprises at closing.

-

Gather your current mortgage details. Pull your most recent mortgage statement. Note your remaining balance, current interest rate, remaining term, and monthly payment. You will use these numbers to compare against new loan options.

-

Check your credit report. Request your free credit report from AnnualCreditReport.com. Dispute any errors before applying, since even a small score improvement can lower your new rate.

-

Compare 10-, 15-, and 20-year refinance options. Each term carries a different rate and monthly payment. 15-year mortgage rates averaged 5.90%–6.09% in mid-2026. That rate difference versus a 30-year loan at 7% or higher can save more than $225,000 in lifetime interest on a $280,000 loan.

-

Calculate monthly payments and total interest for each term. Use a mortgage calculator to model each scenario side by side. The goal is to find the term that maximizes interest savings without pushing your monthly payment beyond what your budget can support.

-

Estimate closing costs and calculate your break-even point. Closing costs typically run 2%–5% of the loan amount. On a $280,000 loan, that is $5,600–$14,000 upfront. Divide that figure by your monthly savings to find how many months until you come out ahead.

-

Apply with a reputable lender. Submit your application with full documentation: W-2s, tax returns, pay stubs, and bank statements. The Texas Mortgage Pros connects homeowners with over 70 lenders, which means you get competing offers rather than a single take-it-or-leave-it quote.

-

Adjust your budget for the higher payment. Before closing, build the new payment into your monthly budget. If the increase feels tight, revisit whether a 20-year term offers a better balance between savings and affordability.

-

Close the refinance and start your new payment schedule. At closing, your original loan is paid off and your new shorter-term loan begins. Refinancing starts a fresh amortization schedule; it does not carry forward any credit from your previous payments.

The table below shows how term length affects a $280,000 refinance at representative 2026 rates:

| Loan Term | Approximate Rate | Monthly Payment (P&I) | Total Interest Paid |

|---|---|---|---|

| 30-year | 7.00% | $1,863 | $390,680 |

| 20-year | 6.50% | $2,088 | $221,120 |

| 15-year | 6.00% | $2,364 | $145,520 |

| 10-year | 5.75% | $3,066 | $87,920 |

Note: Payment figures are illustrative estimates for comparison purposes.

Pro Tip: Ask each lender for a Loan Estimate within three business days of applying. Federal law requires this document, and it lets you compare rates, fees, and closing costs across lenders on an apples-to-apples basis.

How does refinancing compare to making extra principal payments?

Refinancing to a shorter term is not the only way to pay off your mortgage faster. Adding extra principal payments to a 30-year mortgage can cut 7–10 years off the loan term and save tens of thousands of dollars in interest. The key difference is flexibility.

With extra payments, you choose how much to add each month. If your income drops or an unexpected expense hits, you simply stop the extra payments with no penalty. A refinance locks you into a higher mandatory payment every single month.

Here is how the two strategies compare across the factors that matter most:

| Factor | Shorter-term refinance | Extra principal payments |

|---|---|---|

| Monthly payment | Higher, fixed, mandatory | Flexible, optional |

| Closing costs | 2%–5% of loan amount | None |

| Interest rate | Lower new rate possible | Existing rate stays |

| Payoff acceleration | Guaranteed by loan structure | Depends on consistency |

| Best for | Homeowners with stable income | Homeowners wanting flexibility |

Extra payments work best when your current interest rate is already competitive, your income varies, or you want to avoid the upfront cost of closing. Refinancing wins when you can lock in a meaningfully lower rate and commit to the higher payment long term.

One scenario where extra payments clearly beat refinancing: you are 15 years into a 30-year loan. Refinancing into a new 30-year mortgage at that point resets your payoff date and increases total interest paid, even if the new rate is lower. Extra payments on your existing loan preserve the progress you have already made.

For homeowners managing tighter budgets, part-time income strategies can help fund extra principal payments without requiring a full refinance commitment.

What mistakes should you avoid when shortening your mortgage term?

The most expensive mistake in term reduction refinancing is choosing the wrong new term. Many homeowners refinance into a fresh 30-year loan to lower their monthly payment without realizing they are extending their payoff date and adding years of interest. Always compare the total interest paid over the life of the new loan against what remains on your current loan.

- Skipping the break-even calculation. If you move or sell before reaching the break-even point, you lose money on the refinance. Break-even for term reduction refinancing is measured by the crossover point where total interest on the new loan falls below the remaining interest on the old loan.

- Underestimating the payment increase. A 15-year payment on a $280,000 loan is several hundred dollars more per month than a 30-year payment. Homeowners who do not budget for this increase risk missing payments or carrying high-interest credit card debt to compensate.

- Ignoring closing costs. Closing costs of 2%–5% are real money. Rolling them into the loan balance increases the amount you owe and reduces your net savings.

- Not shopping multiple lenders. A single lender quote gives you no leverage. Comparing offers from multiple lenders is one of the most direct ways to reduce your rate and fees.

- Refinancing too early in your current loan. If you are only two years into a 30-year mortgage, a shorter-term refinance may make strong sense. But if you are 20 years in, the math often favors extra payments over a full refinance.

“Refinancing completely replaces your original loan with a new amortization schedule. It does not carry forward previous payments or loan age. Every dollar of progress you made on your old loan disappears from the timeline the moment you close on the new one.”

That reality makes timing critical. The longer you have been paying down your current loan, the more carefully you need to model whether a refinance actually saves money versus simply accelerating extra payments.

Key Takeaways

Shorten mortgage term refinancing saves the most money when you lock in a lower rate, stay in the home past the break-even point, and confirm the higher monthly payment fits your budget.

| Point | Details |

|---|---|

| Rate gap triggers refinancing | Pursue a shorter-term refinance when your current rate is at least 0.75–1 percentage point above market rates. |

| Break-even is non-negotiable | Divide closing costs by monthly savings; only refinance if you will stay in the home past that date. |

| Term choice drives total savings | A 15-year loan can save $225,000+ in interest versus a 30-year on a $280,000 balance. |

| Extra payments offer flexibility | Adding principal to your existing loan cuts 7–10 years off a 30-year term with no closing costs. |

| Avoid resetting the clock | Refinancing into a new 30-year loan after many years on your original loan increases total interest paid. |

What I have learned from helping homeowners shorten their mortgage terms

Working with homeowners on term reduction refinancing, the pattern I see most often is this: people focus entirely on the monthly payment and forget to model the total cost. A homeowner who drops from a 30-year to a 15-year loan will pay more each month, and that number gets all the attention. What gets ignored is the $150,000 or more in interest that quietly disappears from the lifetime cost of the loan.

The second thing I have noticed is that the break-even calculation feels abstract until you put real numbers on paper. When a homeowner sees that $8,000 in closing costs is recovered in 28 months, and they plan to stay in the home for another 12 years, the decision becomes obvious. The math does the persuading.

My honest recommendation: do not treat refinancing and extra payments as competing options. They solve different problems. Refinancing locks in a lower rate and a guaranteed payoff date. Extra payments preserve flexibility. If your rate is already low and your income varies, extra payments are the smarter move. If you can lock in a rate that is a full point below what you are paying now, a shorter-term refinance is hard to beat.

The homeowners who get the best outcomes are the ones who review their mortgage term options proactively, not just when rates make headlines. Set a calendar reminder to review your loan every 12 months. Rates shift, your equity grows, and your financial situation changes. The right move today may not have been the right move two years ago.

— Michelle

How The Texas Mortgage Pros can help you refinance to a shorter term

Deciding between a 10-, 15-, or 20-year refinance takes more than a quick online search. The Texas Mortgage Pros gives you access to over 70 lenders, which means real competing offers rather than a single rate you have to accept or walk away from. Our team walks you through every step, from pulling your credit to comparing Loan Estimates side by side.

Use our mortgage calculators to model your break-even point, compare term lengths, and see exactly how much interest you could save before you ever speak to a lender. When you are ready to move forward, our refinance specialists help you find the right term for your goals and budget. Visit our Texas refinance page to get started with a free consultation today.

FAQ

What is a shorter loan term refinance?

A shorter loan term refinance replaces your existing mortgage with a new loan that has a reduced repayment period, such as moving from 30 years to 15 years. It typically lowers your interest rate and total interest paid while increasing your monthly payment.

How much can I save by refinancing to a 15-year mortgage?

Refinancing from a 30-year loan at 7% or higher to a 15-year loan can save more than $225,000 in lifetime interest on a $280,000 balance. The exact savings depend on your current rate, new rate, and remaining loan balance.

What are typical closing costs for a term reduction refinance?

Closing costs typically range from 2% to 5% of the loan amount. On a $280,000 loan, that equals $5,600–$14,000, which you recover over time through monthly interest savings.

Is it better to refinance or make extra principal payments?

Refinancing wins when you can lock in a rate at least 0.75–1 percentage point lower and plan to stay in the home past the break-even point. Extra principal payments are better when your current rate is already competitive or your income varies month to month.

Does refinancing reset my mortgage term?

Yes. Refinancing completely replaces your original loan with a new amortization schedule and does not carry forward any credit from previous payments. Choosing a shorter new term is the only way to avoid extending your payoff date.