My First Texas Home loan steps define a structured path to down payment assistance and a low-interest mortgage for first-time buyers in Texas. The program, administered by the Texas Department of Housing and Community Affairs (TDHCA), connects eligible buyers with approved lenders who handle both the first mortgage and the assistance funds in a single process. Following these steps correctly means the difference between a smooth closing and weeks of preventable delays. This guide covers every stage, from eligibility checks to closing day, with practical tips built for Texas buyers in 2026.

What prerequisites are required before starting My First Texas Home?

Eligibility is the first gate. The My First Texas Home program defines a first-time homebuyer as someone who has not owned a home in the past three years. Active military veterans are exempt from this rule and may qualify regardless of prior ownership.

Your credit score is the next factor. Most Texas programs require a minimum score of 620, though some loan types accept lower scores when compensating factors like strong income or low debt are present. The average credit score in Texas was 692 as of 2025, so many buyers already meet the baseline without extra preparation.

Income limits and purchase price caps also apply and vary by county. A household in Travis County faces different thresholds than one in Lubbock County, so you must verify the limits for your specific area through the TDHCA website before assuming you qualify. Exceeding the income cap by even a small amount disqualifies you from the program.

Here is what you need to confirm before contacting a lender:

- No homeownership in the past three years (or active military status)

- Credit score of 620 or higher (verified, not estimated)

- Household income within TDHCA county limits

- Purchase price within program caps for your county

- Property must be your primary residence

Pro Tip: Pull your free credit reports from AnnualCreditReport.com at least 60 days before applying. Errors on credit reports are common, and disputing them takes time. Catching a mistake early protects your score and your timeline.

How do you find and work with an approved lender?

You cannot apply directly to TDHCA. Applications must go through authorized participating lenders who are approved to reserve program funds on your behalf. Working with an unauthorized lender means you lose access to the down payment assistance entirely, even if you meet every other requirement.

The distinction between pre-qualification and full pre-approval matters more than most first-time buyers realize. Pre-qualification is an informal estimate based on self-reported numbers. Full pre-approval requires income documentation, a hard credit pull, and asset verification. Sellers in competitive Texas markets prioritize buyers with full pre-approvals because the offer carries verified financial backing. In a multiple-offer situation, a pre-qualification letter is often ignored.

Gather these documents before your first lender meeting:

- Two years of W-2s or tax returns (self-employed buyers need two years of returns)

- Recent pay stubs covering the last 30 days

- Two to three months of bank and investment account statements

- Government-issued photo ID

- Social Security number for credit authorization

- Documentation of any gift funds being used toward the purchase

Verify your lender’s participation status directly through the TDHCA-approved lender list on the TDHCA website. Do not rely on a lender’s verbal claim that they are approved. The list is publicly available and updated regularly.

Pro Tip: Request a Loan Estimate from at least two or three approved lenders within a 14-day window. Multiple credit inquiries for the same loan type within that period count as a single inquiry on your credit report, so shopping around costs you nothing in score impact.

What is the homebuyer education requirement?

Homebuyer education is mandatory for most Texas down payment assistance programs, including My First Texas Home. At least one borrower on the loan must complete a HUD-approved homebuyer education course before closing. This is not optional, and lenders will not proceed to closing without the certificate.

Courses run 4–8 hours and typically cost $50–$100. Both online and in-person formats are accepted, so scheduling is flexible. Certificates remain valid for 12–24 months depending on the provider, which gives you a reasonable window between completing the course and closing on your home.

The most common mistake buyers make is treating this requirement as an afterthought. Scheduling delays in education can push back the entire loan approval and closing timeline. If a popular in-person course is booked out for three weeks, your closing date moves with it.

The education itself is genuinely useful. Topics include budgeting for homeownership costs, understanding mortgage terms, maintaining a home, and knowing your rights as a buyer. Buyers who complete the course report feeling more confident about the financial responsibilities that follow the keys being handed over.

- Register for a HUD-approved course as soon as you decide to buy

- Keep your completion certificate in a dedicated folder with your other loan documents

- Confirm certificate validity dates with your lender at the start of the process

- Online courses through providers like eHome America and Framework are widely accepted

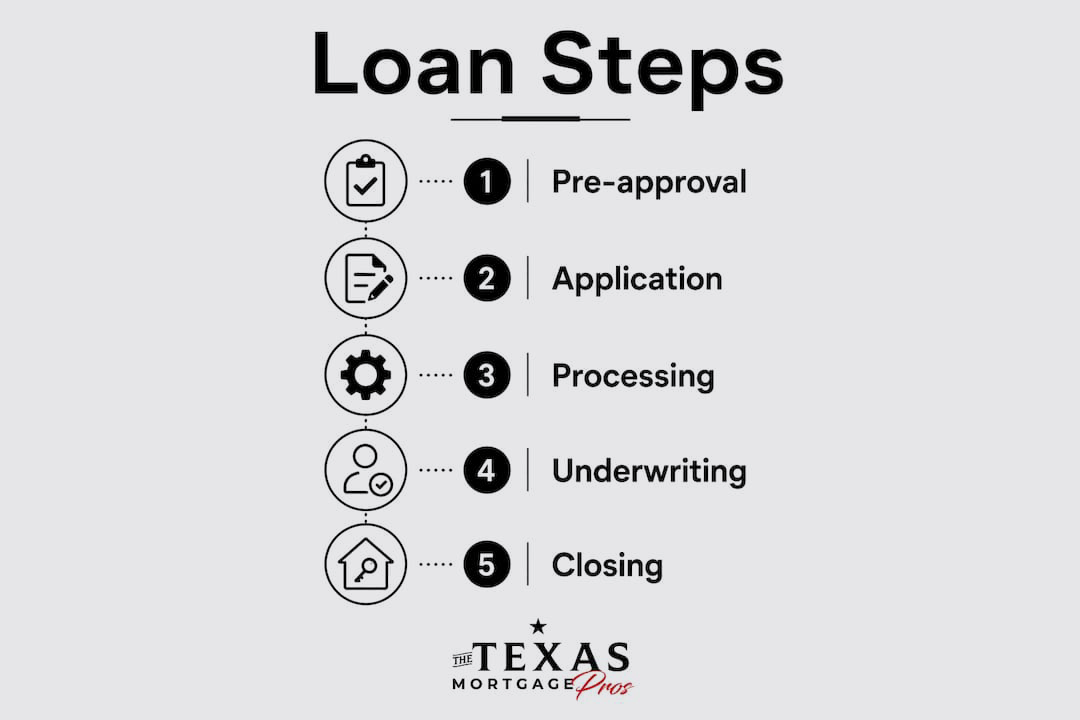

Step-by-step overview: from application to closing

The Texas home loan process follows a defined sequence. Understanding each stage helps you anticipate what comes next and avoid surprises.

| Stage | Action Required | Typical Timeline |

|---|---|---|

| Pre-approval | Submit documents, credit pull, lender review | 3–7 business days |

| Home search | Work with a real estate agent, make an offer | Varies by market |

| Contract signing | Executed purchase agreement triggers next steps | Day 1 of closing clock |

| Lender submission | Full loan file submitted for processing | Days 1–10 |

| Underwriting | Lender verifies all documents and conditions | Days 10–25 |

| Condition clearing | Respond to underwriter requests promptly | Days 25–40 |

| Closing | Sign documents, funds disburse, keys transfer | Days 30–55 |

The typical timeline from contract signing to closing for My First Texas Home loans is 30 to 55 days. Program layers add 1 to 2 weeks to a standard mortgage closing, so build that buffer into your planning when negotiating a closing date with the seller.

Down payment assistance funds are reserved by your lender after the purchase contract is signed. TDHCA-approved lenders handle both the first mortgage and the assistance application in a single process, removing the burden of coordinating two separate applications. The down payment assistance is structured as a 0% interest second mortgage, forgivable after three years of occupancy. If you sell or refinance within three years, the assistance must be repaid.

At closing, you sign the loan documents, the title transfers, and the DPA funds are disbursed directly to cover your down payment and eligible closing costs. Down payment assistance typically covers up to 5% of the mortgage loan, which translates to roughly $9,300 to $15,500 for median-priced Texas homes, given the current median home price of approximately $310,000.

Pro Tip: Respond to every underwriter condition request within 24 hours. Slow responses are the single most common cause of closing delays. Keep your phone and email accessible during the underwriting phase.

What mistakes should first-time Texas buyers avoid?

Avoidable errors cause most closing delays and disqualifications. Knowing them in advance puts you ahead of most first-time buyers.

- Waiting too long on homebuyer education. Treating it as a last-minute checkbox is the most common timing mistake. Complete it before you start seriously touring homes.

- Applying with a non-approved lender. Any lender not on the TDHCA authorized list cannot process your assistance funds. Verify participation before submitting any documents.

- Submitting incomplete documentation. Missing a single bank statement or unsigned form sends your file back to the start of underwriting. Organize every document before submission.

- Relying on pre-qualification instead of pre-approval. Pre-qualification does not carry weight in a competitive offer situation. Get the full pre-approval before you start making offers.

- Ignoring income and credit limits. A raise, a new credit card, or a large purchase between pre-approval and closing can shift your eligibility. Avoid major financial changes during the loan process.

“The buyers who close on time are the ones who treat the loan process like a job. They respond fast, stay organized, and ask questions early rather than late.”

Understanding these pitfalls before you start is worth more than any checklist. The My First Texas Home program rewards prepared buyers. Unprepared ones face delays, resubmissions, and sometimes disqualification.

Key Takeaways

Completing My First Texas Home loan steps requires meeting eligibility criteria, working with a TDHCA-approved lender, finishing homebuyer education early, and staying organized through underwriting to close on time.

| Point | Details |

|---|---|

| Eligibility comes first | Confirm credit score, income limits, and first-time buyer status before contacting any lender. |

| Use only approved lenders | Only TDHCA-authorized lenders can reserve down payment assistance funds on your behalf. |

| Complete education early | HUD-approved courses take 4–8 hours; scheduling delays can push back your entire closing date. |

| Full pre-approval wins offers | Verified pre-approval carries far more weight than pre-qualification in competitive Texas markets. |

| DPA is forgivable after 3 years | The 0% interest second mortgage is forgiven if you stay in the home for three years without selling or refinancing. |

What I have learned from watching buyers go through this process

The buyers who struggle most with the My First Texas Home process are not the ones with the lowest credit scores. They are the ones who underestimate how much preparation the program actually requires.

I have seen buyers with strong finances lose their preferred closing date because they registered for homebuyer education the week of closing. I have seen others submit a loan file to a lender who was not on the approved list and had to start over from scratch. Both situations are entirely avoidable.

The pre-approval step is where I see the biggest mindset shift. Buyers who walk into the home search with a full pre-approval letter carry themselves differently. They make faster decisions, their offers get taken seriously, and they close with less stress. Getting that full mortgage pre-approval early is not just a procedural step. It changes how the entire transaction goes.

My honest advice is to treat document organization as seriously as the home search itself. Create a dedicated folder, digital or physical, with every required document ready before your first lender call. Buyers who do this move through underwriting faster and close more quickly than their target date. The process is manageable when you respect the sequence.

— Michelle

How The Texas Mortgage Pros supports your home loan application

The Texas Mortgage Pros works with a network of over 70 lenders, including TDHCA-approved lenders who can process My First Texas Home applications from pre-approval through closing. First-time buyers get direct access to experts who know the program requirements, the documentation checklist, and the timing details that keep closings on track.

Use the mortgage payment calculators to estimate your monthly payment and confirm your budget before you start the application. When you are ready to move forward, the team can walk you through available Texas down payment assistance programs and connect you with an approved lender who fits your situation. Get your free mortgage quote and take the first concrete step toward your Texas home.

FAQ

Q: What is the minimum credit score for My First Texas Home?

A: The program requires a minimum credit score of 620 for most loan types. Some loan options may accept lower scores when strong compensating factors are present.

Q: How much down payment assistance can I receive?

A: Assistance covers up to 5% of the mortgage loan amount. For a median-priced Texas home at approximately $310,000, that translates to roughly $9,300 to $15,500 toward your down payment and closing costs.

Q: Can I apply directly to TDHCA for the loan?

A: No. You must apply through an authorized participating lender. TDHCA does not accept direct applications from buyers.

Q: How long does the My First Texas Home closing process take?

A: Closing typically takes 30–55 days after the purchase contract is signed. Program requirements add one to two weeks beyond a standard mortgage timeline.

Q: Is the homebuyer education course required for every borrower?

A: At least one borrower on the loan must complete a HUD-approved course. Courses run 4–8 hours and cost $50–$100, with both online and in-person options available through providers like eHome America and Framework.