Mortgage pre-approval is a lender’s formal, verified offer to loan you a specific amount based on your documented income, assets, credit history, and debt load. Unlike a casual estimate, it carries real weight because the lender has reviewed your actual financial records. According to Zillow’s 2024 survey data, 94% of mortgage buyers get pre-approved before making an offer, making it a near-universal step in the homebuying process. The Consumer Financial Protection Bureau (CFPB) and NerdWallet both confirm that pre-approval gives you a concrete budget and strengthens your position with sellers before you ever tour a home.

What is mortgage pre-approval vs. pre-qualification?

These two terms sound similar, but they represent very different levels of commitment from a lender. Understanding the distinction saves you from wasting time or losing a home to a better-prepared buyer.

Pre-qualification is informal. You provide self-reported income and debt figures, and the lender gives you a rough estimate of what you might borrow. No documents change hands, and no credit check occurs. It takes minutes and costs nothing, but sellers treat it as little more than a guess.

Pre-approval is a different process entirely. As NerdWallet confirms, pre-approval is verified with actual documentation and a hard credit inquiry. The lender reviews your tax returns, pay stubs, bank statements, and credit report before issuing a letter with a specific loan amount. That letter tells sellers you are a serious, qualified buyer.

Here is a side-by-side comparison:

| Feature | Pre-qualification | Pre-approval |

|---|---|---|

| Documentation required | None | Tax returns, pay stubs, bank statements, ID |

| Credit check | Soft or none | Hard inquiry |

| Lender commitment | Informal estimate | Conditional loan offer |

| Seller credibility | Low | High |

| Time to complete | Minutes | 1 to 3 business days |

- Pre-qualification works well for early budget planning, before you are ready to shop.

- Pre-approval is what you need when you are actively searching for a home.

- In competitive Texas markets, sellers routinely reject offers that arrive without a pre-approval letter.

Pro Tip: Ask your lender whether your pre-approval file passed automated underwriting. Files that clear automated underwriting carry less risk of denial at the final approval stage.

What documents and steps does the pre-approval process require?

The mortgage pre-approval process follows a clear sequence. Knowing what to gather in advance cuts the timeline significantly and reduces back-and-forth with your lender.

According to NerdWallet’s documentation guidance, lenders typically require two years of tax documents, recent pay stubs, bank statements, and a government-issued ID. Self-employed borrowers should also prepare profit and loss statements and business tax returns. Having these documents organized before you apply is the single fastest way to speed up your approval.

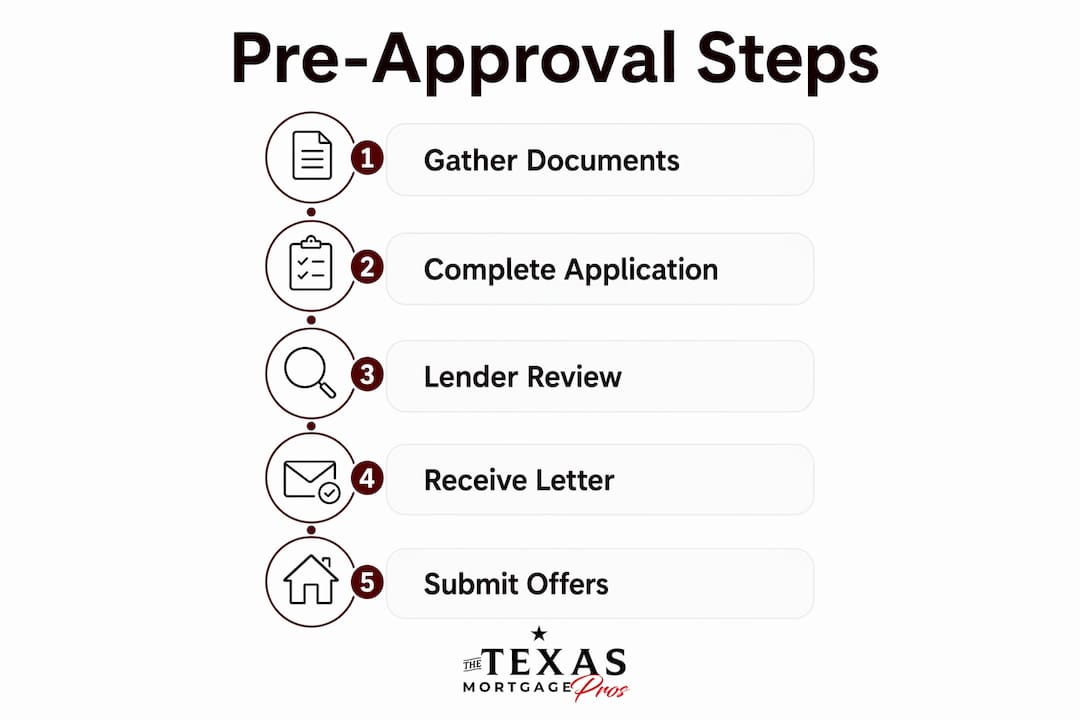

Here are the standard mortgage pre-approval steps:

- Check your credit score. Review your credit report through AnnualCreditReport.com before applying. Dispute any errors, since inaccuracies can lower your score and reduce your loan amount.

- Gather your financial documents. Collect W-2s and 1099s for the past two years, your two most recent pay stubs, two to three months of bank statements, and a valid photo ID.

- Choose a lender and submit your application. You can apply with banks, credit unions, or mortgage brokers. See our guide on choosing the right lender before committing to one.

- Authorize the hard credit inquiry. The lender pulls your full credit report. This temporarily lowers your score by a few points, but multiple mortgage inquiries within a 45-day window count as a single inquiry under FICO scoring rules.

- Receive your pre-approval letter. The CFPB reports that lenders typically issue letters within 1 to 3 business days, and those letters are valid for 60 to 90 days.

For a full breakdown of every document you may need, the mortgage application documents guide from The Texas Mortgage Pros covers each item in detail.

Pro Tip: Apply with two or three lenders on the same day. Because FICO groups mortgage inquiries within a 45-day window, your credit score takes only one hit while you collect multiple offers to compare rates.

What are the benefits and limitations of mortgage pre-approval?

Pre-approval gives you two concrete advantages: a defined budget and negotiating power. Both matter more than most first-time buyers realize.

On the budget side, your pre-approval letter states the maximum loan amount a lender will offer. This prevents you from falling in love with a $450,000 home when your actual ceiling is $380,000. Zillow notes that pre-approval letters help buyers focus their search on realistically priced listings and negotiate from a position of strength. Sellers and their agents take pre-approved buyers far more seriously than those who arrive with only a pre-qualification estimate.

The limitations are equally real, and ignoring them creates problems later.

- Pre-approval is not a final loan guarantee. The CFPB is explicit that a pre-approval letter is conditional. Property appraisal and full underwriting still determine whether the loan closes.

- Letters expire. Most pre-approval letters are valid for 60 to 90 days. If your home search runs long, you will need to reapply and submit updated documents.

- Your financial profile must stay stable. Opening a new credit card, financing a car, or changing jobs between pre-approval and closing can trigger a re-review or outright denial.

- The approved amount is a ceiling, not a recommendation. Being approved for $500,000 does not mean you should spend $500,000. Factor in property taxes, insurance, and maintenance when setting your real budget.

A pre-approval letter opens the door, but it does not close the deal. The final loan approval depends on the property’s appraised value, a clean title search, and your financial situation remaining unchanged from application to closing.

When should you get pre-approved and how do you stay eligible?

Timing your pre-approval correctly prevents two common problems: letter expiration and last-minute financial surprises. The CFPB recommends getting pre-approved close to your home search start, ideally within 90 days of when you plan to make offers. Starting too early means your letter expires before you find the right home. Starting too late means you lose homes to buyers who already have letters in hand.

Staying eligible after pre-approval requires deliberate financial discipline. The CFPB warns that new debt after pre-approval can jeopardize your final loan approval. That means no new credit cards, no auto loans, no large cash withdrawals, and no job changes between pre-approval and closing.

Here is what to do during the active search period:

- Keep all existing accounts current and pay every bill on time.

- Avoid making large deposits that cannot be documented, since underwriters will ask about the source.

- Do not co-sign any loans for family members or friends.

- Notify your loan officer immediately if your employment situation changes.

- Use your pre-approval letter as a shopping tool. The CFPB confirms that a pre-approval is not a commitment to use that lender, so you can still compare rates and fees before choosing where to close.

For guidance on getting the best rate once you are pre-approved, review these Texas mortgage rate tips before locking in.

Pro Tip: Before your letter expires, ask your lender what a renewal requires. Some lenders only need updated pay stubs and a new credit pull. Knowing this in advance prevents a frantic scramble if your search runs past 90 days.

Key takeaways

Mortgage pre-approval is a lender-verified conditional offer that defines your buying power, strengthens your offers, and requires you to maintain financial stability from application through closing.

| Point | Details |

|---|---|

| Pre-approval vs. pre-qualification | Pre-approval uses verified documents and a hard credit check; pre-qualification is self-reported and informal. |

| Required documents | Gather two years of tax returns, recent pay stubs, bank statements, and a valid ID before applying. |

| Timeline and validity | Lenders issue letters within 1 to 3 business days; letters expire in 60 to 90 days. |

| Not a final guarantee | Property appraisal and underwriting still determine whether the loan closes after pre-approval. |

| Financial stability matters | New debt, job changes, or large unexplained deposits after pre-approval can trigger denial. |

Why pre-approval timing changed how I advise buyers

Most first-time buyers treat pre-approval as a checkbox. They get the letter, feel confident, and then make financial decisions that quietly unravel the whole process. I have seen buyers lose their loan approval in the final week because they financed furniture for the new home before closing. The lender pulled a final credit check, found the new installment account, and the debt-to-income ratio no longer qualified.

The advice I give every buyer now is this: treat your finances as frozen from the moment you apply. No new accounts, no large purchases, no job changes. Your financial profile on the day you apply is the profile the underwriter expects to see on closing day.

The other thing most articles skip is the automated underwriting question. Not all pre-approvals carry the same reliability. A letter backed by automated underwriting approval is far stronger than one issued after a manual review of your documents. Ask your loan officer directly: “Did my file pass automated underwriting?” If the answer is yes, your path to closing is considerably smoother.

Finally, use your pre-approval letter as leverage, not just proof of financing. In a competitive Texas market, submitting an offer with a strong pre-approval letter from a recognized lender signals to the seller that you will not fall through. That credibility has closed deals at the same price when competing offers came in slightly higher but with weaker financing documentation.

— Michelle

Start your pre-approval with The Texas Mortgage Pros

The Texas Mortgage Pros works with a network of over 70 lenders to find competitive rates that fit your financial profile, whether you are a first-time buyer, a veteran, or purchasing an investment property.

Use our mortgage calculators to estimate your monthly payment based on your pre-approval amount and current rates. If you are ready to take the next step, explore first-time homebuyer programs in Texas that may reduce your down payment or closing costs. Our loan officers guide you from document gathering through closing, so you never face the process alone. Get your free mortgage quote today and see what you qualify for.

FAQ

What is mortgage pre-approval in simple terms?

Mortgage pre-approval is a lender’s conditional offer to loan you a specific amount after reviewing your income, credit, and financial documents. It tells sellers you are a qualified buyer and defines your realistic home shopping budget.

How long does mortgage pre-approval take?

Most lenders issue a pre-approval letter within 1 to 3 business days after you submit your complete application and documents. Having your tax returns, pay stubs, and bank statements ready in advance speeds up the process.

What is the difference between pre-qualification and pre-approval?

Pre-qualification is an informal estimate based on self-reported financial information with no credit check. Pre-approval requires verified documents and a hard credit inquiry, making it far more credible to sellers and real estate agents.

How long is a mortgage pre-approval letter valid?

Pre-approval letters are typically valid for 60 to 90 days. If your home search extends beyond that window, you will need to reapply with updated financial documents and a new credit pull.

Can I get pre-approved by multiple lenders?

Yes, and doing so is a smart strategy. A pre-approval letter is not a commitment to use that lender, so you can compare rates and fees across multiple lenders. Multiple mortgage inquiries within a 45-day period count as a single inquiry under FICO scoring rules, protecting your credit score.