Mortgage rates fluctuate daily because they are directly tied to the trading of Mortgage-Backed Securities (MBS) in the bond market, not to any single government decision. When investors buy and sell MBS, yields shift, and lenders reprice their rate sheets to match. Economic reports on inflation, employment, and consumer spending trigger these MBS trades throughout the day, meaning the rate you see at 9 a.m. may not be the rate available at 2 p.m. Understanding why mortgage rates change gives you a real edge when timing your purchase or refinance.

Why mortgage rates fluctuate daily: the MBS connection

Mortgage-Backed Securities are bundles of home loans sold to investors on the bond market. When you take out a mortgage, your lender typically sells that loan into an MBS pool, freeing up capital to lend again. The price investors pay for those securities determines the yield, and that yield sets the baseline for new mortgage rates.

Daily rate movements often range from 0.01% to 0.08%, driven by economic reports such as jobs data. That may sound small, but on a $350,000 loan, a 0.08% swing changes your monthly payment by roughly $17 and your total interest cost by more than $6,000 over 30 years. Small daily shifts compound into real money.

When MBS prices rise, yields fall, and mortgage rates drop. When MBS prices fall, yields rise, and rates climb. This inverse relationship is the core mechanic behind every daily rate variation you see quoted online. You can read more about how MBS instruments work and why they differ from other loan types.

On volatile trading days, the repricing cycle accelerates sharply. Lenders may reprice three to four times before noon, updating their rate sheets each time. This means a rate quoted to you in the morning can be outdated by the time you call back after lunch.

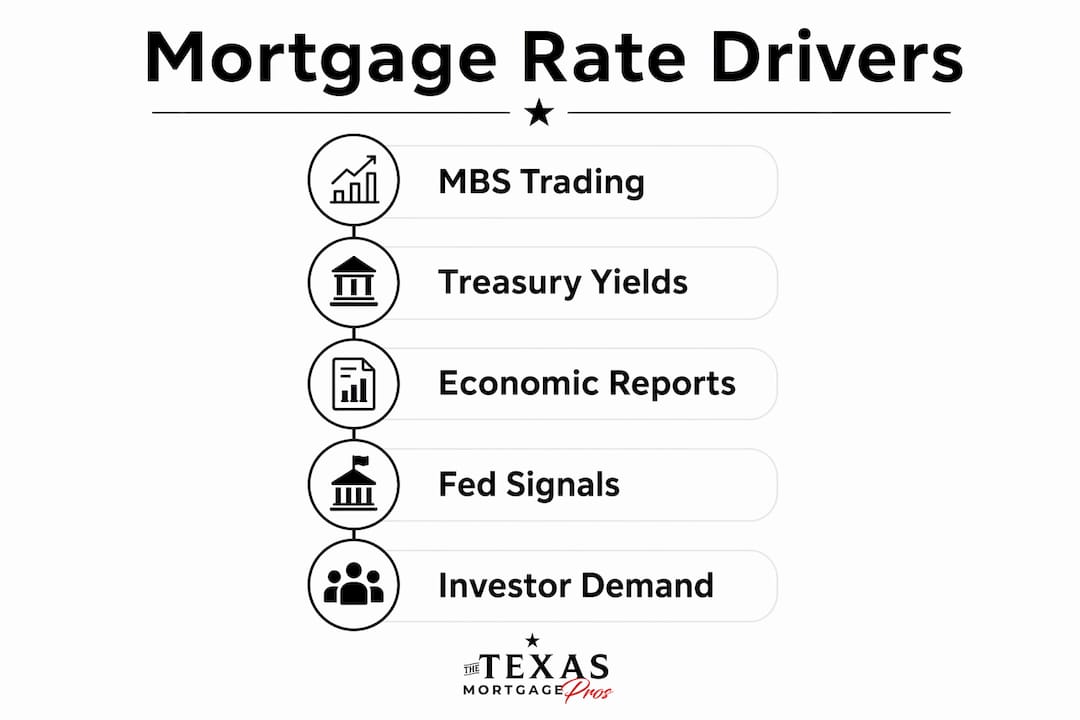

Key factors that trigger MBS price swings during a single trading day include:

- Jobs reports: A stronger-than-expected payroll number signals economic growth, which raises inflation fears, pushes bond prices down, and lifts mortgage rates.

- CPI releases: Inflation data moves bond markets faster than almost any other report.

- Federal Reserve speeches: Even informal comments from Fed officials shift investor expectations and trigger immediate MBS repricing.

- Geopolitical events: Uncertainty drives investors toward safe assets like U.S. Treasuries, which indirectly affects MBS demand.

Pro Tip: Ask your lender what time they release their daily rate sheet. Calling right after the morning sheet drops, before any repricing, gives you the most accurate quote for that day.

How Treasury yields shape mortgage rate trends

The 10-year U.S. Treasury note yield is the most widely tracked benchmark for mortgage rate trends. It does not set mortgage rates directly, but it moves in close parallel because both instruments compete for the same pool of fixed-income investors.

Mortgage rates run approximately 1.50% to 1.75% above the 10-year Treasury yield. Investors demand that premium because mortgages carry prepayment risk. Homeowners can refinance or sell at any time, cutting off the investor’s income stream early. That uncertainty requires compensation above the risk-free Treasury rate.

The table below shows how this spread plays out at different Treasury yield levels:

| 10-year Treasury yield | Typical 30-year mortgage rate | Approximate spread |

|---|---|---|

| 3.50% | 5.00%–5.25% | 1.50%–1.75% |

| 4.00% | 5.50%–5.75% | 1.50%–1.75% |

| 4.50% | 6.00%–6.25% | 1.50%–1.75% |

| 5.00% | 6.50%–6.75% | 1.50%–1.75% |

When the federal government issues large amounts of new Treasury debt, the increased supply pushes existing bond prices down and yields up. Higher Treasury yields pull mortgage rates upward with them. Inflation expectations work the same way. If investors believe inflation will erode the purchasing power of future bond payments, they demand higher yields to compensate, and mortgage rates follow. Tracking the 10-year Treasury yield on any financial news platform gives you a reliable early signal of where mortgage rates are heading that day.

What economic reports and Fed signals move rates the most

The Federal Reserve does not directly set mortgage rates. The Fed manages short-term interest rates through the federal funds rate, which influences bank lending costs and market expectations. Mortgage rates are set by bond market investors pricing long-term inflation risk, not by Fed committee votes. This distinction matters because many buyers wait for a Fed rate cut expecting immediate mortgage relief, only to find rates unchanged or even higher.

The reports that actually move mortgage rates on a daily basis are the ones that change investor expectations about inflation and economic growth. Inflation data like CPI can push mortgage rates up or down by 0.125% to 0.25% in a single day. A 3.3% year-over-year CPI reading, for example, triggered immediate bond market volatility and sharp mortgage rate shifts when it was released. That is a full rate tier change in one morning.

The major economic releases that cause daily rate variability include:

- Consumer Price Index (CPI): The single most market-moving report for mortgage rates. Higher-than-expected inflation sends rates up immediately.

- Producer Price Index (PPI): A leading indicator of future consumer inflation; bond markets react before CPI confirms the trend.

- Non-Farm Payrolls (NFP): Released the first Friday of each month, this jobs report is the second most impactful event for mortgage rates. Strong hiring signals wage growth and inflation pressure.

- Average Hourly Earnings: Embedded in the NFP report, wage growth data moves rates independently because rising wages feed consumer spending and inflation.

- GDP reports: Quarterly but significant. A stronger-than-expected GDP reading pushes rates higher; a weak reading can pull them lower.

- Fed meeting minutes and speeches: Even off-cycle remarks from Federal Open Market Committee members shift bond yields within minutes of publication.

The practical takeaway is that you should know the economic calendar before locking a rate. Locking the day before a major CPI release is a calculated risk. If inflation comes in hotter than expected, rates could jump before your lender processes the lock.

Why your rate differs from the market rate

Even when the bond market holds steady all day, two borrowers applying at the same lender on the same morning can receive different rate quotes. Individual mortgage rates combine the base market rate set by MBS pricing with lender margins that reflect borrower risk, loan type, and market competition. The market rate is the floor, not the final number.

Lenders also manage something called pipeline risk. When a lender’s loan pipeline fills up, processing capacity tightens. Lenders adjust rates to slow incoming applications when their pipeline is full, effectively pricing themselves out of the market temporarily. This means you could get a higher quote from a busy lender than from a competitor with open capacity, even on the same day with identical market conditions.

Here is how borrower-specific factors layer onto the base market rate:

- Credit score: A score above 740 typically earns the best available pricing. Scores below 680 can add 0.50% or more to your rate through risk-based pricing adjustments.

- Down payment: Putting down less than 20% usually requires private mortgage insurance and triggers higher rate tiers. A 10% down payment costs more than a 20% down payment, even at the same lender.

- Loan types: Conventional, FHA, VA, and jumbo loans each price differently relative to MBS benchmarks. VA loans often carry lower rates because the government guarantee reduces investor risk.

- Property type: Investment properties and second homes carry rate premiums of 0.50% to 0.75% above primary residence rates.

- Rate lock length: A 60-day lock costs more than a 30-day lock because the lender carries more market risk during the longer period.

Rate locks protect borrowers from daily market fluctuations but typically last 30 to 60 days. Delays in processing may require a lock extension, which carries fees and can expose you to the current market rate if the lock expires. Understanding your lender’s lock policy before you go under contract is one of the most practical steps you can take.

Pro Tip: Compare mortgage deal structures from at least three lenders on the same day for an apples-to-apples comparison. Rates quoted on different days reflect different market conditions, not differences between lenders.

Key takeaways

Mortgage rates move daily because MBS trading, Treasury yields, and economic data all shift investor expectations in real time, and lender-specific pricing layers on top of those market signals.

| Point | Details |

|---|---|

| MBS trading drives daily changes | Bond market buying and selling of MBS sets the baseline for lender rate sheets each day. |

| Treasury yields are the benchmark | Mortgage rates run 1.50%–1.75% above the 10-year Treasury yield as a standard spread. |

| CPI and jobs data move rates fast | Inflation and employment reports can shift rates by 0.125%–0.25% within a single trading session. |

| The Fed sets expectations, not rates | Fed policy influences bond market sentiment indirectly; the bond market sets actual mortgage rates. |

| Your profile adjusts the market rate | Credit score, down payment, and loan type add or subtract from the base rate every lender quotes. |

What I’ve learned about watching rates without losing your mind

After working with hundreds of Texas homebuyers, I can tell you that the biggest mistake I see is obsessing over daily rate movements to the point of paralysis. Rates moved up 0.04% today. They dropped 0.03% yesterday. Neither number tells you whether this is a good week to lock.

What actually matters is the rate trend over weeks, not the noise of any single day. If the 10-year Treasury yield has climbed 0.30% over the past three weeks, that is a signal worth acting on. A 0.04% daily blip is not.

I also think buyers underestimate how much the lock conversation matters. Many people ask their lender, “What’s the rate?” without asking, “How long is this rate good for and what happens if my closing is delayed?” Those are the questions that protect you. A rate that looks great on Monday can expire before your closing date if you did not ask about extension terms upfront.

The other thing I have seen cost buyers real money is shopping rates across different days instead of the same day. You call Lender A on Tuesday and Lender B on Thursday. The market moved between those calls, and now you think Lender B is cheaper, even though they might actually be identical. Always compare lenders on the same day to get a clean comparison.

Daily fluctuations are real, but they are manageable. Work with someone who monitors the market actively and tells you when conditions favor locking. That guidance is worth more than any single rate quote.

Lock in your rate with confidence through The Texas Mortgage Pros

Rate volatility does not have to slow down your home purchase. The Texas Mortgage Pros works with a network of over 70 lenders to find competitive pricing tailored to your specific loan profile, whether you are a first-time buyer, a veteran, or refinancing an existing home.

Use our mortgage calculators to see exactly how daily rate changes affect your monthly payment before you lock. When you are ready for a real number, get a free rate quote based on today’s market. Our team monitors MBS pricing and economic releases daily so you get guidance grounded in what the market is actually doing, not what it did last week.

FAQ

What causes mortgage rates to change every day?

Mortgage rates change daily because they are tied to Mortgage-Backed Securities trading in the bond market, which responds to economic reports, inflation data, and investor sentiment in real time. Events like CPI releases or jobs reports can shift rates by 0.125% to 0.25% within a single session.

Does the Federal Reserve control mortgage rates?

No. The Fed manages short-term borrowing costs through the federal funds rate, but mortgage rates are set by bond market investors pricing long-term inflation expectations. A Fed rate cut does not guarantee lower mortgage rates.

How many times can a lender change rates in one day?

On volatile trading days, lenders may reprice three to four times before noon. Each repricing reflects new MBS pricing from the bond market, so a morning quote can be outdated by the afternoon.

How does a rate lock protect me from daily fluctuations?

A rate lock freezes your quoted rate for a set period, typically 30 to 60 days, shielding you from market moves during loan processing. If your closing is delayed beyond the lock period, extension fees apply and you may face current market rates if the lock expires.

Why is my mortgage rate different from my neighbor’s?

Even with identical market conditions, two borrowers receive different rates because lenders price each loan based on credit score, down payment, loan type, and property use. These risk adjustments layer on top of the base market rate set by MBS trading.

Recommended

- Why Homebuyers Are Turning to Adjustable Rate Mortgages in Today’s Market – The Texas Mortgage Pros

- Marry The House, Date The Rate: Smart or Flawed Homebuying Strategy? – The Texas Mortgage Pros

- How Interest Rates Affect Texas First-Time Home Buyers – The Texas Mortgage Pros

- Mortgage Calculators – The Texas Mortgage Pros