An FHA loan in Texas is a government-insured mortgage that gives first-time homebuyers access to financing with as little as 3.5% down and flexible credit requirements. The Federal Housing Administration backs these loans, which means lenders take on less risk and can offer terms that conventional financing rarely matches for buyers without large savings or perfect credit. Texas buyers in Austin, Houston, Dallas, and beyond use FHA loans to close on homes they could not otherwise afford. If you have been waiting on the sidelines because of your credit score or down payment, this guide covers exactly what you need to know.

What are the FHA loan requirements in Texas?

FHA loan requirements in Texas follow federal guidelines set by the Department of Housing and Urban Development, with a few details shaped by local market conditions. Meeting these requirements is more achievable than most first-time buyers expect.

Credit score and down payment thresholds

The credit score floor for an FHA loan is 580 for the standard 3.5% down payment. Buyers with scores between 500 and 579 can still qualify, but they must bring 10% down instead. By comparison, conventional loans require 620 as a minimum credit score, which locks out a significant portion of first-time buyers. That gap makes FHA the practical choice for anyone still building their credit profile.

Debt-to-income ratio and employment

Texas FHA loans allow a debt-to-income ratio up to 43%, with exceptions reaching 50% when compensating factors apply. Compensating factors include cash reserves, a strong employment history, or a larger down payment. Lenders also require steady employment, typically two years in the same field, along with verifiable income through pay stubs, W-2s, or tax returns. Self-employed buyers can qualify using two years of tax returns showing consistent earnings.

2026 FHA loan limits by Texas county

| County Type | 2026 Loan Limit (Single-Family) |

|---|---|

| Standard Texas counties | $541,287 |

| High-cost counties (e.g., Collin) | Up to $563,500+ |

2026 FHA loan limits in Texas range from approximately $541,287 in standard counties to over $563,500 in high-cost areas like Collin County. These limits reflect rising home prices across the state and give buyers in competitive markets more purchasing power than in prior years.

Pro Tip: Check the HUD website or ask your lender for the exact limit in your specific county before you start shopping. Limits vary by county and property type, and knowing your ceiling prevents wasted time on homes outside your FHA range.

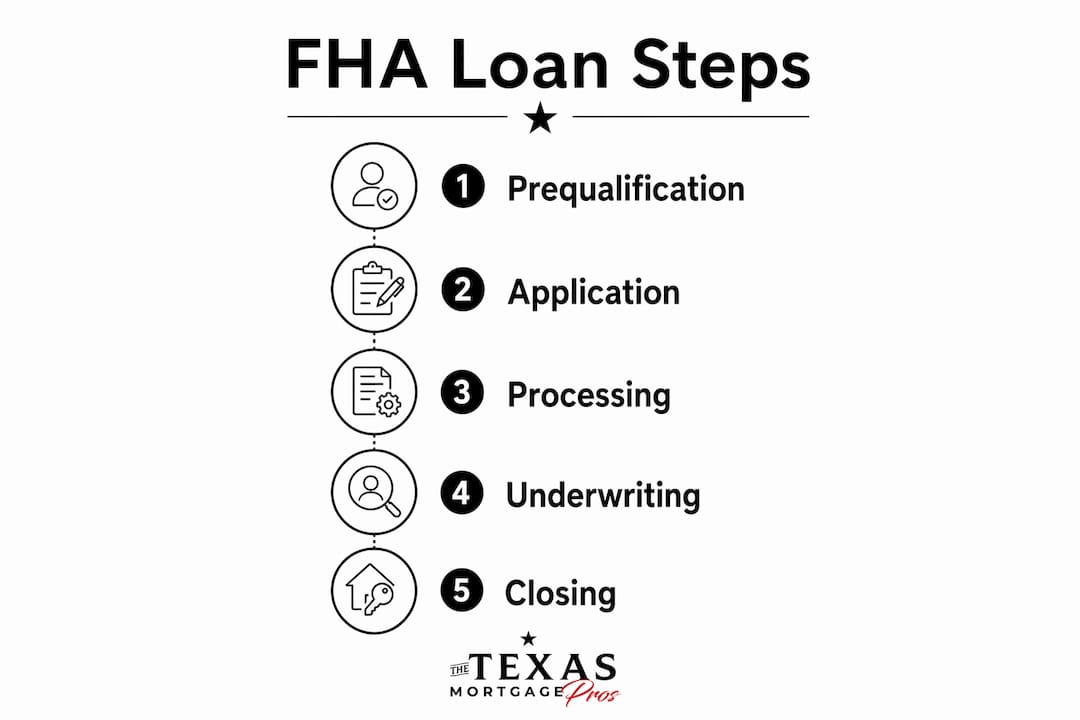

How does the FHA loan application process work in Texas?

Applying for a Texas FHA mortgage follows a clear sequence. Knowing each step in advance reduces delays and keeps your closing on schedule.

- Get pre-approved first. Pre-approval tells you exactly how much you can borrow and signals to sellers that you are a serious buyer. You will submit income documents, bank statements, and authorization for a credit pull at this stage.

- Gather your documentation. Lenders need two years of W-2s or tax returns, recent pay stubs covering 30 days, two months of bank statements, and a government-issued ID. Documentation flexibility in income, debts, and gift funds can significantly help first-time buyers during underwriting, especially when working with a lender experienced in FHA guidelines.

- Choose an FHA-approved lender. Not every lender offers FHA loans, and experience matters. A lender who processes FHA files regularly knows how to handle underwriting questions quickly, which protects your closing date.

- Submit your full application. Once you have an accepted offer on a home, your lender orders an FHA appraisal. The appraisal confirms the property meets HUD’s minimum property standards and establishes its market value.

- Clear underwriting conditions. The underwriter reviews your full file and may request additional documents. Responding within 24 to 48 hours keeps the process moving. Most FHA loans in Texas close within 30 to 45 days from full application.

- Close on your home. At closing, you sign final documents, pay your down payment and closing costs, and receive the keys.

Pro Tip: If a family member is gifting part of your down payment, prepare a signed gift letter stating the funds are not a loan. FHA loans allow gift funds toward both down payment and closing costs, but the paper trail must be clean before underwriting will approve it.

FHA loans vs. conventional loans in Texas: which is better?

The right choice depends on your credit score, savings, and how long you plan to stay in the home. Here is how the two programs compare directly.

| Feature | FHA Loan | Conventional Loan |

|---|---|---|

| Minimum credit score | 500 (580 for 3.5% down) | 620 |

| Minimum down payment | 3.5% | 3% to 5% |

| Mortgage insurance | MIP for 11 years or life of loan | PMI, removable at 20% equity |

| Debt-to-income limit | Up to 50% with exceptions | Typically 45% |

| Gift funds for down payment | Allowed | Allowed with restrictions |

| Seller concessions | Up to 6% of purchase price | Up to 3% to 9% depending on LTV |

The most significant long-term cost difference between FHA and conventional loans is mortgage insurance. FHA loans carry a mortgage insurance premium, known as MIP, which includes an upfront fee and annual payments lasting 11 years or the life of the loan depending on your down payment size. Removing MIP typically requires refinancing into a conventional loan once you have built sufficient equity. Private mortgage insurance on a conventional loan, by contrast, cancels automatically when your loan balance drops to 80% of the home’s value.

The initial loan-to-value ratio on a 3.5% down FHA loan sits at approximately 96.5%, which is why mortgage insurance terms matter so much for your total cost calculation. Buyers who put down 10% on an FHA loan reduce MIP duration to 11 years rather than the full loan term, which meaningfully improves long-term affordability.

On the rate side, FHA loans tend to carry interest rates equal to or lower than conventional loans, which keeps monthly payments competitive even for buyers with credit scores in the 580 to 620 range. For a buyer who cannot yet qualify for conventional financing, FHA is not a consolation prize. It is the right tool for the situation, with a clear path to refinancing once equity grows.

You can explore the FHA vs. conventional comparison in more detail to see which program fits your specific numbers.

What down payment assistance programs work with FHA loans in Texas?

Texas offers some of the most accessible homebuyer assistance programs in the country, and most of them layer directly on top of FHA financing. FHA loans combined with Texas assistance programs create pathways for families who would otherwise be priced out of the market entirely.

The two primary state-level programs are:

- Texas State Affordable Housing Corporation (TSAHC): TSAHC offers grants and forgivable second liens covering up to 5% of the loan amount for down payment and closing costs. The grant option requires no repayment at all, making it the most direct form of assistance available to Texas buyers.

- Texas Department of Housing and Community Affairs (TDHCA): TDHCA runs the My First Texas Home program, which pairs a 30-year FHA loan with a zero-interest second mortgage covering down payment and closing cost assistance. Income and purchase price limits apply, but they are generous enough to cover most first-time buyers in mid-size Texas cities.

Beyond state programs, Texas first-time homebuyer programs frequently provide forgivable loans or grants that cover down payment and closing costs. Cities like Houston, Austin, and San Antonio run their own local assistance funds that stack on top of state programs in some cases. In Houston, the Harvey Homebuyer Assistance Program has provided grants to qualifying buyers in targeted neighborhoods. Austin’s Down Payment Assistance Program offers forgivable loans to buyers meeting income limits.

Seller concessions add another layer of flexibility. FHA loans allow sellers to contribute up to 6% of the purchase price toward the buyer’s closing costs. In a buyer-friendly negotiation, this can eliminate most out-of-pocket closing expenses entirely.

Pro Tip: Stack programs where possible. A TSAHC grant combined with seller concessions can reduce your cash to close to near zero on an FHA purchase. Ask your lender specifically about 2026 assistance programs before you assume you need to come in with the full 3.5% yourself.

Key takeaways

An FHA loan in Texas is the most accessible path to homeownership for first-time buyers because it combines low down payments, flexible credit standards, and compatibility with state and local assistance programs.

| Point | Details |

|---|---|

| Credit score flexibility | Scores as low as 580 qualify for 3.5% down; 500 to 579 requires 10% down. |

| 2026 loan limits | Standard Texas counties allow up to $541,287; high-cost counties exceed $563,500. |

| Mortgage insurance cost | MIP lasts 11 years with 10% down or the full loan term with 3.5% down. |

| Assistance programs available | TSAHC and TDHCA offer grants and forgivable loans that stack with FHA financing. |

| Refinancing as an exit | Refinancing into a conventional loan removes MIP once you reach sufficient equity. |

Why FHA loans still make sense for Texas buyers in 2026

By Gerry Nicodemus

After years of working with first-time buyers across Texas, I have watched a lot of people talk themselves out of FHA loans because of the mortgage insurance. That instinct is understandable, but it is usually wrong for buyers who are just starting out.

The math is straightforward. If you are sitting on a 600 credit score and $15,000 in savings, an FHA loan gets you into a home today. A conventional loan keeps you renting for another two or three years while you save more and repair your credit. The cost of waiting, in rent paid and home price appreciation missed, almost always exceeds the cost of MIP.

What I tell buyers is this: use FHA to get in, build equity, and refinance when your loan-to-value ratio and credit score support a conventional product. That is not a compromise. That is a strategy. The buyers I have seen succeed fastest are the ones who stopped waiting for perfect conditions and used the tools available to them right now.

Texas-specific assistance programs make this even more compelling in 2026. TSAHC and TDHCA have updated their income limits and grant amounts, and stacking those with an FHA loan can genuinely reduce your cash to close to a few thousand dollars. If you are not asking your lender about these programs, you are leaving money on the table.

Work with someone who knows FHA guidelines inside and out. The difference between a lender who processes two FHA files a month and one who processes twenty is the difference between a smooth closing and a stressful one.

— Gerry Nicodemus

Ready to explore your FHA loan options in Texas?

The Texas Mortgage Pros works with a network of over 70 lenders to find competitive rates and terms for first-time buyers across the state, whether you are looking at home loans in Austin, an FHA loan in Houston, or financing anywhere else in Texas.

Use our mortgage calculator to estimate your monthly payment based on current 2026 rates, then connect with our team for a personalized pre-qualification review. We will walk you through every available assistance program, confirm your eligibility, and fight for the rate that fits your budget. Visit The Texas Mortgage Pros to get started or check today’s rates before your first conversation with a lender.

FAQ

What credit score do I need for an FHA loan in Texas?

A credit score of 580 qualifies you for the standard 3.5% down payment option. Scores between 500 and 579 still qualify but require a 10% down payment instead.

What are the 2026 FHA loan limits in Texas?

Standard Texas counties have a 2026 FHA loan limit of approximately $541,287 for a single-family home. High-cost counties like Collin County exceed $563,500, with limits varying by property type.

How long does MIP last on a Texas FHA loan?

MIP duration depends on your down payment. With 3.5% down, MIP lasts the life of the loan. With 10% or more down, MIP ends after 11 years. Refinancing into a conventional loan is the most common way to remove it earlier.

Can I use down payment assistance with an FHA loan in Texas?

Yes. Programs through TSAHC and TDHCA offer grants and forgivable second liens that work directly with FHA financing. Seller concessions up to 6% of the purchase price can also offset closing costs.

How long does it take to close an FHA loan in Texas?

Most FHA loans in Texas close within 30 to 45 days from full application submission. Responding quickly to underwriting requests and having your documentation ready at the start shortens that timeline considerably.