A non-QM loan is a mortgage that falls outside Qualified Mortgage standards but remains fully compliant with federal Ability-to-Repay rules under the Dodd-Frank Act. The Consumer Financial Protection Bureau (CFPB) requires every lender to verify a borrower’s ability to repay, regardless of loan type. What changes with non-QM loans is the documentation method, not the legal obligation to underwrite responsibly. For self-employed borrowers, real estate investors, and gig workers, this distinction is the difference between qualifying for a home loan and being turned away entirely. The Texas Mortgage Pros works with over 70 lenders to match borrowers with non-QM options that fit their actual financial picture.

What is a non-QM loan and how does it differ from a QM loan?

A Qualified Mortgage (QM) is a loan that meets specific federal standards set by the CFPB, including a debt-to-income ratio at or below 43%, full income documentation through W-2s and tax returns, and no risky features like interest-only payments or balloon payments. A non-QM mortgage operates outside those standards while still meeting the ATR requirement. The lender must still prove you can repay. They use different evidence to do it.

The most practical difference shows up in documentation. QM loans rely on tax returns and employer verification. Non-QM loans accept alternative documentation such as 12–24 months of bank statements, profit-and-loss statements, Debt-Service Coverage Ratio (DSCR) calculations, or 1099 forms. This matters enormously for borrowers whose taxable income does not reflect their true cash flow.

A common misconception is that non-QM loans are reckless or predatory products. They are not. They represent a structural choice that fits borrowers whose financial lives do not fit a W-2 mold. The underwriting is rigorous. It is simply different.

| Feature | QM Loan | Non-QM Loan |

|---|---|---|

| Income documentation | W-2s, tax returns | Bank statements, 1099s, DSCR, assets |

| Debt-to-income limit | 43% cap | Flexible, case-by-case |

| Interest-only payments | Not allowed | Allowed on select products |

| Consumer protections | Full QM safe harbor | Reduced; ATR compliance required |

| Typical borrower | Salaried employee | Self-employed, investor, gig worker |

Pro Tip: If your tax returns show significantly less income than your bank deposits, ask a lender to run a bank statement qualification side by side with a conventional one. The difference in loan size can be substantial.

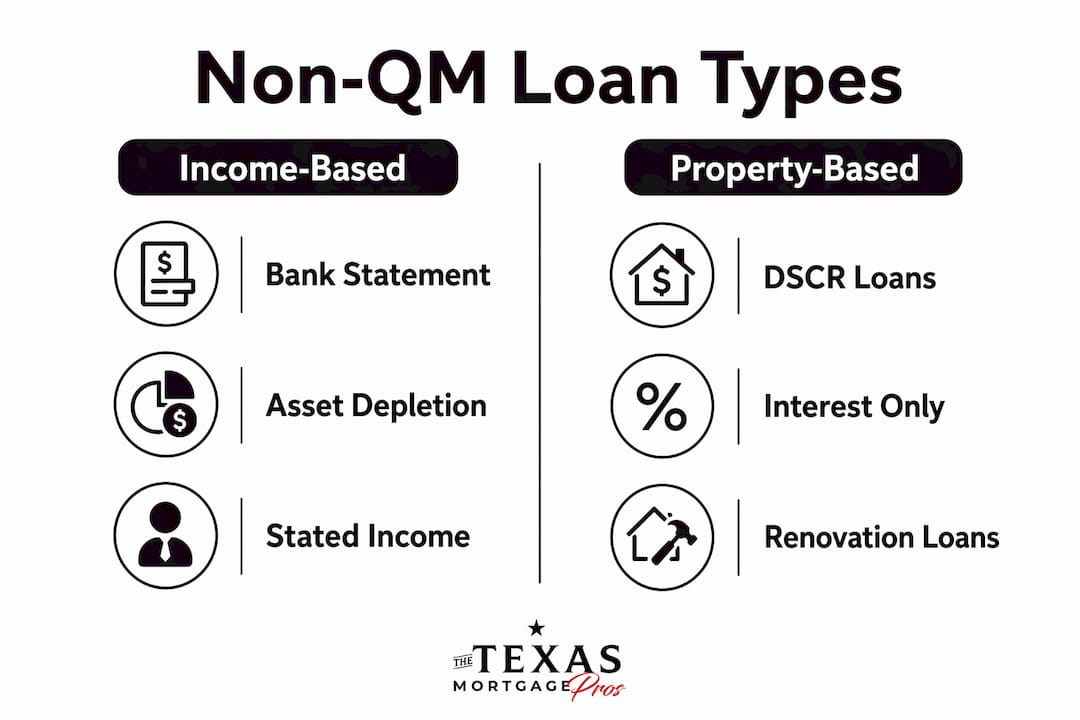

What are the main types of non-QM loans?

Non-QM is not a single product. It is a category that covers several distinct loan structures, each designed for a specific borrower profile.

Bank statement loans serve self-employed borrowers who write off significant business expenses. A borrower earning $17,500 per month in deposits but showing only $9,583 in taxable income can qualify for more using bank statement underwriting than they ever could with a conventional loan. Lenders typically average 12–24 months of deposits to calculate qualifying income.

DSCR loans are built for real estate investors. The lender evaluates the property’s rental income rather than the borrower’s personal income. If the property generates enough rent to cover the mortgage payment, the loan qualifies. This makes DSCR loans the go-to product for investors building rental portfolios who do not have personal W-2 income.

1099 loans target independent contractors and gig workers. Platforms like rideshare driving, freelance design, or consulting produce 1099 income that fluctuates year to year. Traditional lenders penalize that variability. Non-QM lenders average it.

Additional non-QM categories include:

- Asset-based loans: Qualification is based on liquid assets rather than income, suited for retirees or high-net-worth borrowers with low reported income.

- Foreign national loans: Designed for non-U.S. citizens purchasing American real estate without a Social Security number or U.S. credit history.

- Interest-only loans: Borrowers pay only interest for a set period, reducing initial monthly payments. Common in high-cost markets.

- Jumbo non-QM loans: Loan amounts above conforming limits with flexible documentation, serving buyers in expensive markets where standard jumbo guidelines are too restrictive.

Each product type requires its own documentation package. Knowing which category fits your situation is the first step toward a successful application. The Texas Mortgage Pros can help you identify the right fit through their non-QM loan programs for nontraditional borrowers.

What do non-QM loans cost, and what are the risks?

Non-QM loans carry a real cost premium. Interest rates run 0.5%–2.0% higher than comparable conventional loans. That premium reflects the additional underwriting complexity and the capital costs lenders absorb by holding these loans outside agency channels. On a $400,000 loan, a 1.5% rate difference adds roughly $350 per month to your payment.

Qualification thresholds are also stricter in some ways. Typical requirements include:

- Minimum credit scores starting at 620, though many lenders prefer 660 or higher

- Down payments ranging from 10%–40%, depending on loan type and credit profile

- Substantial asset reserves, often 6–12 months of mortgage payments

- Loan seasoning requirements on income and assets

Beyond cost, borrowers face specific risks that do not apply to QM products:

- Reduced consumer protections: Non-QM lenders do not receive the same legal safe harbor as QM lenders. This shifts some risk back to the borrower.

- Prepayment penalties: Many non-QM loans include prepayment penalties for the first 1–3 years. Refinancing early can be expensive.

- Adjustable rates: Some non-QM products feature adjustable rate structures that can significantly increase payments after the initial fixed period.

These risks are real and should factor into your decision. A non-QM loan makes financial sense when the premium cost is lower than the cost of waiting or not buying at all.

Pro Tip: Before committing to a non-QM product, calculate the total interest premium over your expected hold period. If you plan to refinance within 24 months, the premium may be worth it. If you plan to hold for 10 years, run the full numbers first.

How do you apply for a non-QM loan?

The application process for a non-QM loan follows a logical sequence. Preparation is the most important step.

- Assemble your alternative documentation package. Gather 12–24 months of personal or business bank statements, a current profit-and-loss statement prepared by a CPA, and any 1099s or asset statements relevant to your loan type. Organized documentation speeds up underwriting significantly.

- Find a lender that specializes in non-QM products. Not every lender offers these loans. Specialty mortgage brokers and portfolio lenders are the most reliable sources. The Texas Mortgage Pros works with a network of over 70 lenders, including those with dedicated non-QM programs.

- Understand the underwriting timeline. Non-QM loans close in 14–21 days on average, faster than the 21–30 days typical for conventional loans. This speed advantage exists because non-QM lenders do not require IRS transcript verification or agency underwriting queues.

- Compare terms across multiple lenders. Rate premiums, prepayment penalty structures, and reserve requirements vary widely between non-QM lenders. Getting at least two or three quotes is standard practice.

- Plan your exit strategy. The most effective use of a non-QM loan is as a bridge. Refinancing after 24 months into a conventional QM product is a common strategy once a borrower has built a qualifying income history or improved their credit profile. Discuss this plan with your lender upfront.

For self-employed borrowers specifically, reviewing your self-employed home loan options before applying gives you a clearer picture of what documentation lenders actually need.

Key Takeaways

Non-QM loans are fully regulated, alternative-documentation mortgages that serve borrowers whose income or financial profile does not fit conventional QM standards, making them a legitimate and practical financing tool for self-employed individuals, investors, and nontraditional earners.

| Point | Details |

|---|---|

| Regulatory compliance | Non-QM loans must meet federal ATR rules; they are not exempt from income verification. |

| Rate premium | Expect to pay 0.5%–2.0% more than a comparable conventional loan rate. |

| Loan types | Bank statement, DSCR, 1099, asset-based, and jumbo non-QM each serve a distinct borrower profile. |

| Qualification criteria | Credit scores typically start at 620; down payments range from 10%–40% depending on the product. |

| Bridge strategy | Plan to refinance into a conventional loan after 24 months to reduce long-term interest costs. |

Why I think non-QM loans are misunderstood more than they are misused

The conversation around non-QM loans tends to go one of two ways. Either borrowers dismiss them as risky subprime products, or they treat them as a workaround that requires no real financial discipline. Both views are wrong.

What I have seen working with borrowers over the years is that non-QM loans are most valuable when the borrower understands exactly why they need one and has a plan for what comes next. A freelance architect earning $180,000 a year who shows $70,000 in taxable income is not a risky borrower. The tax code is working exactly as designed. The problem is that conventional underwriting cannot see past the return.

The real risk I see is borrowers using non-QM products without considering the rate premium over time. A 1.5% premium on a $500,000 loan is $7,500 per year. Over five years, that is $37,500. If you have a realistic path to conventional financing within two years, that math works. If you do not, you need to factor that cost into your purchase decision honestly.

My advice is always the same: use a non-QM loan as a tool with a defined purpose, not as a permanent solution. Build your qualifying income history, protect your credit score, and set a refinance target date before you close. Borrowers who approach it that way consistently come out ahead. Those who treat it as a set-and-forget product often pay more than they need to.

For a deeper look at how these products are structured, the non-QM mortgage breakdown from The Texas Mortgage Pros covers the mechanics clearly.

— Michelle

How The Texas Mortgage Pros can help with non-QM financing

The Texas Mortgage Pros specializes in alternative financing solutions for borrowers who do not fit the conventional mold. Whether you are self-employed, investing in rental properties, or working through a nontraditional income situation, their team connects you with the right lender from a network of more than 70 lenders.

Getting the right non-QM product starts with understanding your numbers. Use the mortgage payment calculator to estimate how different rate scenarios affect your monthly budget. Then check current Texas mortgage rates to see where non-QM pricing sits today. The Texas Mortgage Pros team is available to walk you through your documentation options, compare loan structures, and help you build a financing plan that fits your goals now and in two years.

FAQ

What is a non-QM loan in simple terms?

A non-QM loan is a mortgage that does not meet standard Qualified Mortgage guidelines but still requires the lender to verify your ability to repay. It uses alternative documentation, such as bank statements or rental income, instead of W-2s and tax returns.

Who qualifies for a non-QM loan?

Self-employed borrowers, real estate investors, gig workers, foreign nationals, and high-net-worth individuals with low reported income are the most common non-QM borrowers. Minimum credit scores typically start at 620, with down payments ranging from 10%–40%.

Are non-QM loans riskier than conventional loans?

Non-QM loans carry higher interest rates and fewer consumer protections than QM loans, but they are not inherently reckless. All non-QM lenders must comply with federal Ability-to-Repay rules, which require documented income and asset verification regardless of loan type.

How much more do non-QM loans cost?

Non-QM loan rates run 0.5%–2.0% above comparable conventional loan rates. The exact premium depends on your credit score, down payment, loan type, and thelender’ss specific pricing model.

Can I refinance a non-QM loan into a conventional mortgage later?

Yes. Refinancing into a conventional QM loan after building a qualifying income history is a common strategy. Many borrowers target refinancing after 24 months, once their documented income or credit profile meets standard agency guidelines.