Mortgage application documents needed are specific proofs of your financial status, identity, and property details that lenders require to evaluate your eligibility for a home loan. The formal term for this collection is a loan application package, and getting it right the first time is the single biggest factor in how fast your approval moves. Missing even one document can pause underwriting for days. This guide covers every document category you need, explains what lenders actually do with each one, and flags the mistakes that most often slow down first-time buyers.

What are the essential documents needed for a mortgage application?

Every mortgage application, regardless of loan type, requires the same core categories of documentation. Lenders use these to verify who you are, what you earn, what you own, and what you owe. Think of it as building a financial portrait that a stranger, your underwriter, must trust enough to approve a six-figure loan.

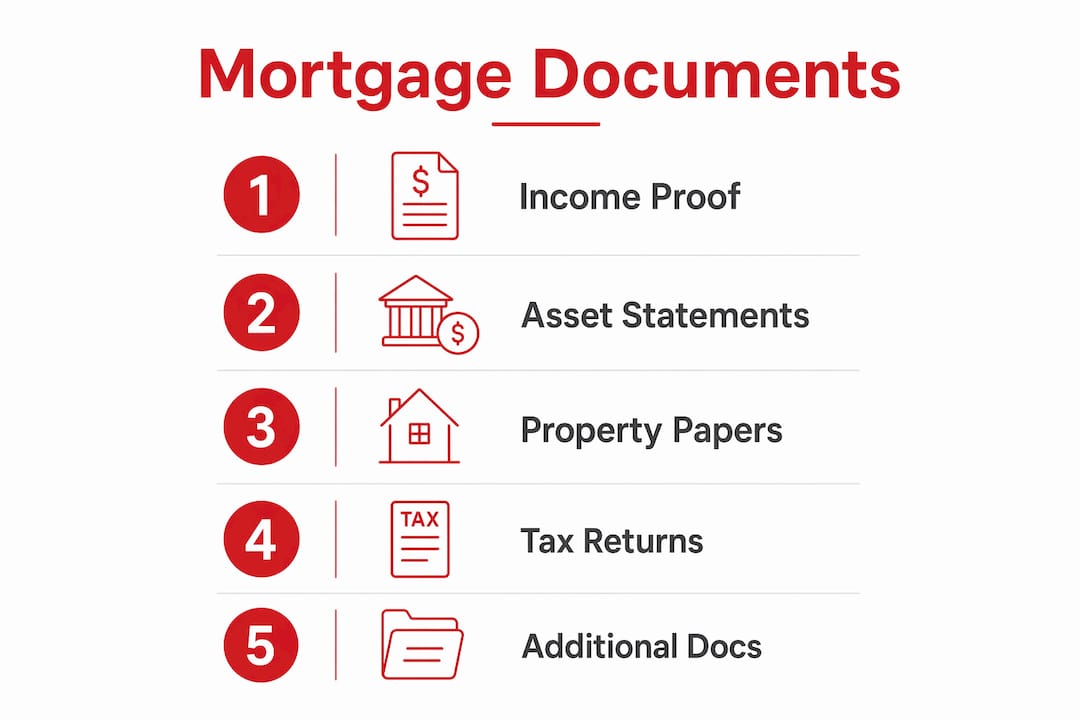

Income verification is the foundation of any loan file. Lenders require pay stubs covering the last 30 days, along with W-2 forms for the past two years. This combination shows both your current earnings and your income stability over time. Tax returns for the last two years round out the picture, especially if you have rental income, investment gains, or other non-salary earnings.

Identity and credit documents are equally non-negotiable:

- Government-issued photo ID (driver’s license or passport)

- Social Security number for credit pull authorization

- Most recent credit report, which lenders typically pull directly

- Signed Form 4506-T, which authorizes the IRS to release your tax transcripts to the lender

Asset documentation proves you have the funds to close. Bank statements for checking, savings, and investment accounts covering the most recent two to three months are standard, and lenders want every page, not just the summary page. These statements verify your down payment source and confirm you have reserves after closing.

Property documents come into play once you are under contract. You will need the signed purchase agreement, the property address, and sometimes a copy of the listing. Your lender will order the appraisal independently, but you may need to provide HOA contact information if the property is in a managed community.

Pro Tip: Gather your last two years of tax returns and W-2s before you even start house hunting. Pre-approval moves much faster when your income documents are already organized and ready to upload.

How do document requirements differ for self-employed borrowers?

Document requirements vary significantly by borrower status, and self-employed applicants face the most complex paperwork requirements. If you own a business or work as a freelancer, lenders cannot simply verify your income with a pay stub. They need a fuller picture of your business finances to confirm that your earnings are stable and likely to continue.

Self-employed borrowers must provide two years of personal and business tax returns, a current profit-and-loss statement, and documentation of business ownership, such as a business license or a CPA letter. Lenders average your net income across two years, so a strong recent year does not automatically offset a weaker prior year. For more on loan options designed around this income structure, the self-employed home loan programs at Thetexasmortgagepros explain how non-QM products can work in your favor.

Other special borrower situations also require additional paperwork:

- Gift funds: A properly formatted gift letter signed by the donor, plus bank statements from both the donor and recipient showing the transfer. The letter must explicitly state the funds are a gift, not a loan.

- Divorce or separation: Divorce decrees, separation agreements, and documentation of alimony or child support payments if those amounts factor into your qualifying income.

- Recent job change: An employment verification letter from your new employer confirming your position, start date, and salary. Lenders want to see that the change was lateral or upward, not a sign of instability.

- 1099 contractors: Two years of 1099 forms plus business bank statements showing consistent deposits over time.

Pro Tip: If you receive gift funds for your down payment, document the transfer as soon as it happens. Mismanagement of gift fund documentation is one of the most common causes of avoidable underwriting delays.

How to organize your mortgage application documents effectively

Organization is not just a convenience. It directly affects how quickly your loan moves through underwriting. A disorganized file forces processors to chase down missing pages, which adds days or weeks to your timeline.

Follow these steps to build a clean, lender-ready document package:

- Create a master folder structure. Set up separate digital folders labeled by category: Income, Assets, Identity, Property, and Other. Use a cloud storage service like Google Drive or Dropbox so you can instantly share access with your loan officer.

- Name every file clearly. Use a consistent format such as “LastName_W2_2024” or “LastName_BankStatement_Chase_Jan2026.” Vague file names like “scan001.pdf” force processors to open every file to find what they need.

- Include every page. Lenders want complete documents. A bank statement that runs four pages must be submitted as four pages. Submitting only the first page is one of the most common reasons files get kicked back.

- Use your lender’s secure portal. Most lenders, including those in the Thetexasmortgagepros network, provide encrypted upload portals. Avoid sending sensitive documents by email unless the lender specifically requests it and uses secure email.

- Keep a personal backup. Save a copy of everything you submit. If a document gets lost in the process or a lender requests a second submission, you can respond within minutes rather than days.

- Check expiration dates. Pay stubs older than 30 days and bank statements older than 60 days are typically considered stale. Refresh these documents close to your application date, not weeks before.

What common mistakes slow down the mortgage application process?

Common errors like missing signatures, unexplained deposits, or mismatched information are the most frequent causes of underwriting delays. Most of these mistakes are entirely preventable with a careful review before you submit.

The errors that cause the most friction include:

- Inconsistent information: Your name, address, and Social Security number must match exactly across every document and your loan application. A middle initial on one form but not another can trigger a manual review.

- Unexplained large deposits: Any deposit that is not a paycheck and exceeds roughly half your monthly income will require a written explanation and source documentation. Move money between accounts before you start the process, not during it.

- Incomplete tax returns: Submitting only the first two pages of a multi-page return is a common mistake. Every schedule and attachment must be included.

- Missing gift letter details: A gift letter that omits the donor’s relationship to you, the exact dollar amount, or the explicit statement that repayment is not expected will be rejected outright.

- Outdated pay stubs: Submitting a pay stub from 60 days ago when the lender needs one from the last 30 days is an easy mistake that adds unnecessary back-and-forth.

“The fastest mortgage approvals we see come from borrowers who treat their document package like a legal filing. Every page present, every signature in place, every number consistent across the entire file.”

Reviewing your documents against your loan application before submission takes about 30 minutes and can save two to three weeks of processing time.

How do lenders use your documents during underwriting?

Underwriting is the verification stage in which a lender’s underwriter cross-checks every document you submitted against the information in your loan application. The formal application form used in this process is the Uniform Residential Loan Application, also known as Form 1003. Underwriting compares the 1003 details against all supporting documents and flags any discrepancy that requires explanation.

Here is what underwriters specifically verify and why each check matters:

| Document reviewed | What the underwriter verifies |

|---|---|

| Pay stubs and W-2s | Confirms income matches the amount stated on the 1003 application |

| Bank statements | Verifies down payment source and checks for undisclosed large deposits |

| Tax returns and Form 4506-T | Cross-checks reported income against IRS records for accuracy |

| Photo ID and Social Security number | Confirms identity and prevents fraud or application errors |

| Purchase agreement | Verifies property address, sale price, and contract terms align with the loan |

Underwriters rigorously cross-check every piece of submitted documentation against the loan application, and even small mismatches require written explanations before the file can move forward. Full disclosure upfront, including any unusual income sources or recent financial changes, is always faster than waiting for the underwriter to find something and ask about it. Working with a loan specialist who reviews your file before submission catches most of these issues before they reach underwriting.

Key takeaways

A complete, consistent, and well-organized mortgage document package is the single most effective way to accelerate your loan approval.

| Point | Details |

|---|---|

| Core documents required | Gather pay stubs, W-2s, tax returns, bank statements, photo ID, and a signed purchase agreement. |

| Self-employed borrowers | Provide two years of business and personal tax returns plus a current profit and loss statement. |

| Gift fund documentation | Submit a signed gift letter and bank statements showing the transfer before applying. |

| Organization matters | Use clearly named digital folders and submit complete documents through your lender’s secure portal. |

| Avoid common errors | Check that names, SSNs, and income figures match exactly across every document and your application. |

What I’ve learned after years of watching mortgage files succeed and fail

I have seen buyers with excellent credit and high incomes have their closings delayed by two weeks because of a single unexplained deposit or a missing page in a bank statement. The paperwork side of a mortgage is not glamorous, but it is where deals actually live or die.

The advice I give every buyer I work with is this: start building your document package at least 60 days before you plan to apply. That window gives you time to request tax transcripts from the IRS if needed, resolve any discrepancies on your credit report, and move funds into the accounts you plan to use for closing without triggering deposit questions.

For self-employed buyers, the stakes are even higher. Two years of business tax returns is the baseline, but lenders also want to see that your business income is trending stable or upward. If your most recent year shows a significant drop, even a temporary one, you may need to explore non-QM mortgage options that use bank statement income instead of tax return income.

The buyers who close on time are not necessarily the ones with the best finances. They are the ones who show up with a clean, complete, and consistent file. That is entirely within your control, and it starts with understanding exactly what your lender needs before you hand anything over.

Ready to apply? Thetexasmortgagepros can guide you through every step

Knowing what documents to gather is the first step. Having a team that reviews your file, spots gaps before underwriting does, and matches you with the right loan program is what gets you to closing on time.

At Thetexasmortgagepros, we work with a network of over 70 lenders to find the loan that fits your situation, whether you are a first-time buyer, a veteran, or self-employed. Use our mortgage payment calculator to estimate your monthly costs before you apply. If you are buying your first home in Texas, explore the first-time homebuyer programs we offer, including down payment assistance options that may reduce what you need to bring to closing. Our loan specialists are ready to review your document package and walk you through the process from pre-qualification to closing day.

FAQ

What documents are needed for a mortgage application?

The standard required mortgage paperwork includes recent pay stubs, two years of W-2s and tax returns, two to three months of bank statements, a government-issued photo ID, your Social Security number, and a signed purchase agreement once you are under contract.

How many months of bank statements do lenders require?

Most lenders require two to three months of bank statements covering all pages of every account, including checking, savings, and investment accounts used for the down payment.

Do self-employed borrowers need extra documents for a mortgage?

Yes. Self-employed applicants must provide two years of personal and business tax returns, a profit and loss statement, and proof of business ownership—lenders average income across both years to determine qualifying income.

What is Form 4506-T and why do lenders need it?

Form 4506-T is an IRS authorization form that allows your lender to request a copy of your tax transcripts directly from the IRS. Lenders require a signed Form 4506-T to verify that the tax returns you submitted match those filed with the IRS.

What happens if my documents have inconsistent information?

Small mismatches in name, SSN, or income between your application and supporting documents will flag a condition in underwriting and require a written explanation before your loan can move forward. Reviewing all documents for consistency before submission prevents this delay.

Recommended

- First-Time Homebuyer Programs in Texas | Service You Can Trust

- Mortgage Calculators – The Texas Mortgage Pros

- The Role Of Loan Specialists In Your Home Buying Team – The Texas Mortgage Pros

- First-Time Home Buyers Guide in Texas – The Texas Mortgage Pros