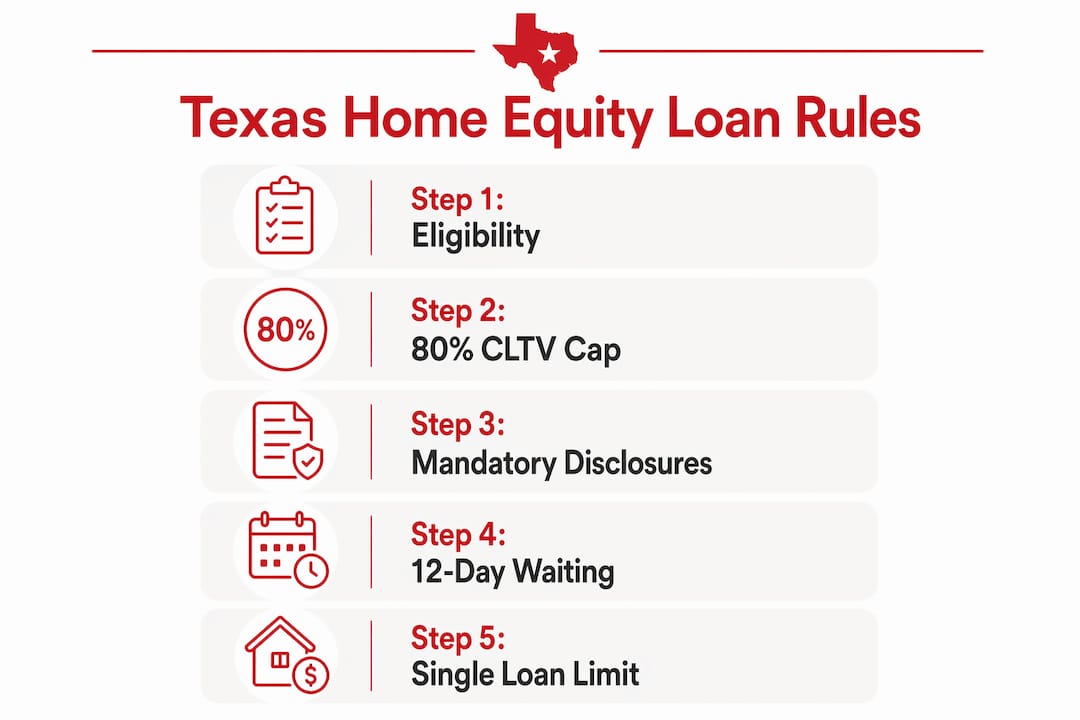

The Texas home equity loan rule is defined under Article XVI, Section 50(a)(6) of the Texas Constitution, making it one of the most protective and restrictive home equity lending frameworks in the United States. Unlike most states, where home equity lending rules are codified in statutes, Texas embeds these protections directly in its constitution. That distinction matters because constitutional provisions are harder to change and carry greater legal weight. For Texas homeowners, this means your home equity borrowing is governed by rules designed to protect you first and lenders second.

What is the Texas home equity loan rule and how does it limit borrowing?

The Texas home equity loan rule sets a hard ceiling: the combined total of all liens secured against your homestead, including your existing mortgage and the new home equity loan, cannot exceed 80% of your home’s fair market value. This is the 80% combined loan-to-value (CLTV) limit, and it applies at the moment the loan is made. It is not a guideline or a soft cap. It is a constitutional requirement.

Here is what that means in practice:

- If your home is worth $400,000, the maximum combined debt allowed is $320,000.

- If you still owe $250,000 on your mortgage, the most you can borrow through a home equity loan is $70,000.

- If you own your home free and clear, you can borrow up to $320,000 on a $400,000 home.

The fair market value used in this calculation is determined at the time of loan origination, typically through a licensed appraisal. This protects both you and the lender from using inflated or outdated valuations. The 20% equity you must retain is not accessible through any home equity product, including a home equity line of credit (HELOC) or cash-out refinance. Texas constitutional protections create some of the strictest home equity loan rules in the country, prioritizing homeowner security over lender flexibility.

Pro Tip: Before applying, calculate your current CLTV by adding your mortgage balance to the loan amount you want, then dividing by your home’s appraised value. If that number exceeds 0.80, you will not qualify under Texas home equity loan guidelines.

What procedural safeguards does Texas law require?

Texas does not just limit how much you can borrow. It also controls how and when the loan can close. These procedural requirements exist to give you time to think, review, and back out if needed. They are not bureaucratic hurdles. They are legal protections built into the process.

- 12-day waiting period. Texas requires a minimum 12-calendar-day wait between the date you submit your application and the date you can close. This period begins when you receive required consumer disclosure notices. No lender can rush you to closing before that window expires.

- Three-day right of rescission. After closing, you have three business days to cancel the loan without penalty. This is a federal protection under the Truth in Lending Act, and Texas fully enforces it. If you change your mind after signing, you can walk away with no financial consequence.

- In-person closing requirement. Texas mandates in-person closing at the lender’s office, a title company, or an attorney’s office. Remote notarization is generally not permitted for home equity loans. This requirement distinguishes Texas from most other states and reinforces that the borrower fully understands what they are signing.

- Fee cap at 2%. Lender fees are capped at 2% of the loan principal. Third-party costs such as appraisals, surveys, and title services are excluded from this cap, but nearly all lender-controlled charges must fall within it. This prevents lenders from loading closing costs onto borrowers.

- One loan at a time. Texas allows only one home equity loan on a homestead at a time. Once you close a home equity loan or cash-out refinance, you must wait 12 months before applying for another. This rule prevents borrowers from stacking debt against their home in rapid succession.

Pro Tip: Mark your calendar from the day you receive your disclosure notices. Lenders cannot waive the 12-day waiting period, and any attempt to close early voids the loan under Texas law.

How do loan structure and documentation requirements work?

Texas home equity loan requirements go beyond borrowing limits and waiting periods. The structure of the loan itself and the paperwork behind it must meet specific constitutional standards.

- Voluntary lien with written consent. The loan must be secured by a voluntary lien created under a written agreement with the consent of all owners and their spouses. If you are married, your spouse must sign even if they are not on the title. This protects both parties from being blindsided by a lien on the family home.

- No blanks in the contract. Texas law prohibits substantive blanks in home equity loan agreements. Every material term must be filled in before you sign. Lenders who leave blanks risk the loan being unenforceable, which is why precise paperwork completion is a priority for every compliant lender.

- Equal monthly installments. Repayments must be in substantially equal installments starting no later than two months after the loan date. Each payment must cover at least the accrued interest. This structure eliminates balloon payments and protects you from payment shock later in the loan term.

- Limited lender recourse. If you default, the lender’s only remedy is judicial foreclosure on the homestead lien. Texas law limits lender recourse to foreclosure only, meaning you cannot be personally sued for a deficiency judgment. This is a significant protection that most other states do not offer.

- No acceleration for market drops. A lender cannot call your loan due simply because your home’s value has fallen or because you have other unrelated debts. Acceleration is prohibited under those circumstances, giving you stability even in a declining market.

How do home equity loans compare to HELOCs and cash-out refinancing in Texas?

All three products let you access your home’s equity, but they work differently and carry distinct trade-offs under Texas home equity rules.

| Feature | Home Equity Loan | HELOC | Cash-Out Refinance |

|---|---|---|---|

| Disbursement | Lump sum upfront | Revolving credit line | Lump sum, replaces mortgage |

| Rate type | Fixed | Variable | Fixed or variable |

| 80% CLTV cap | Yes | Yes | Yes |

| Payment structure | Equal monthly installments | Variable, based on draws | New mortgage payment |

| One-at-a-time rule | Yes | Yes | Yes |

| Best for | Large one-time expenses | Ongoing or flexible needs | Lowering rate while accessing equity |

Both home equity loans and HELOCs share the 80% combined LTV cap under Texas law, so neither product gives you more borrowing room than the other. The key difference is how you receive and repay the funds. A home equity loan provides a fixed amount with predictable payments, which suits homeowners looking to fund a specific project, such as a renovation or debt payoff. A HELOC works more like a credit card, letting you draw and repay repeatedly during the draw period, which suits ongoing or unpredictable expenses.

A cash-out refinance in Texas replaces your existing mortgage with a new, larger loan and gives you the difference in cash. It is subject to the same 80% CLTV cap and one-loan-at-a-time rule. The advantage is that you may be able to lower your interest rate at the same time you access equity. The trade-off is that you restart your mortgage term and pay closing costs on the full loan amount. Understanding which product fits your situation requires considering your current rate, your timeline, and the flexibility you need in repayment.

Key takeaways

Texas home equity loans are constitutionally governed, capped at 80% CLTV, and protected by mandatory waiting periods, fee caps, and limited lender recourse, making them among the most borrower-friendly products in the country.

| Point | Details |

|---|---|

| 80% CLTV hard cap | All liens combined cannot exceed 80% of your home’s fair market value at origination. |

| 12-day waiting period | Closing cannot occur before 12 calendar days after the delivery of the application and disclosure. |

| Fee cap protection | Lender fees are capped at 2% of the loan principal, excluding third-party costs. |

| One loan at a time | Only one home equity product is allowed per homestead, with a 12-month gap between loans. |

| No deficiency judgments | Lenders can only pursue judicial foreclosure, not personal liability, on a defaulted loan. |

Why the Texas home equity rules deserve more respect than they get

I have worked with Texas homeowners long enough to see a consistent pattern: most borrowers come in focused entirely on the interest rate and completely unprepared for the procedural requirements. The 12-day waiting period catches people off guard when they are trying to close quickly. The in-person closing requirement surprises borrowers who assumed they could sign remotely. And the one-loan-at-a-time rule has derailed more than a few homeowners who tried to pull equity twice in the same year.

What I want homeowners to understand is that these rules are not obstacles. They are protections that work in your favor. The fee cap alone can save you thousands compared to what lenders charge in states without similar limits. The prohibition on deficiency judgments means your personal finances are shielded even in a worst-case scenario. No other state gives you that combination of protections at the constitutional level.

The practical lesson is this: plan your borrowing timeline carefully. If you think you might need access to equity again within 12 months, consider whether a HELOC is a better fit than a lump-sum loan. If you are refinancing and want to pull cash out, keep in mind that the same rules apply. And if you are married, make sure your spouse is ready to sign at closing, as their consent is required. The homeowners who navigate this process smoothly are the ones who understand the rules before they apply, not after.

How Thetexasmortgagepros can help you access your home equity

Thetexasmortgagepros works with a network of over 70 lenders to secure competitive home loan rates in Texas that comply with all constitutional requirements. Whether you are exploring a home equity loan, a HELOC, or a cash-out refinance, our team walks you through the 80% CLTV calculation, the waiting period timeline, and the documentation requirements so nothing slows down your closing.

Use our mortgage calculators to estimate your borrowing capacity based on your home’s current value and outstanding mortgage balance. Then connect with one of our loan specialists for a personalized consultation. We handle the paperwork, coordinate with title companies, and keep your timeline on track from application to closing. Get pre-qualified today and take the first step toward accessing your equity with confidence.

FAQ

What is the 80% rule for Texas home equity loans?

The 80% rule means the combined total of all liens on your homestead, including your mortgage and home equity loan, cannot exceed 80% of your home’s fair market value at the time the loan is made. This is a constitutional requirement, not a lender preference.

How long do I have to wait before closing a Texas home equity loan?

Texas requires a minimum 12-calendar-day waiting period after you submit your application and receive required disclosure notices. No lender can waive or shorten this period under any circumstances.

Can I have two home equity loans on my Texas home at the same time?

No. Texas law allows only one home equity loan or cash-out refinance on a homestead at a time. You must also wait 12 months after closing one before applying for another.

What fees can a lender charge on a Texas home equity loan?

Lender fees are capped at 2% of the loan principal. Third-party costs such as appraisals, title services, and surveys are excluded from this cap but must be disclosed upfront.

What happens if I default on a Texas home equity loan?

If you default, the lender’s only legal remedy is judicial foreclosure on the homestead lien. Texas law prohibits deficiency judgments, meaning the lender cannot sue you personally for any remaining balance after foreclosure.

Recommended

- Texas FHA Home Loans: What You Need To Know – The Texas Mortgage Pros

- Home Loans in Texas at Competitive Rates

- First-Time Homebuyer Programs in Texas | Service You Can Trust

- 5 Best Home Loan Programs for the Texas Self-Employed – The Texas Mortgage Pros