A mortgage broker is a licensed intermediary who connects borrowers with multiple lenders to find the home loan that best fits their financial profile. The role of a mortgage broker goes well beyond rate shopping. Brokers assess your credit and income, compare wholesale lenders, manage your application from start to finish, and advocate for you through underwriting and closing. For Texas homebuyers, first-time buyers, veterans, and anyone refinancing, working with a broker means having a knowledgeable professional in your corner rather than navigating dozens of lender options alone.

What does a mortgage broker do throughout the loan process?

A mortgage broker follows a four-stage process that spans weeks or months: financial assessment, lender comparison, application management, and closing support. Each stage involves specific tasks that most borrowers never see but that directly affect whether your loan closes on time and at the best available rate.

Here is what that process looks like in practice:

- Financial and credit assessment. The broker reviews your income, assets, credit score, and debt-to-income ratio before approaching any lender. This profiling determines which loan programs you qualify for and which lenders are most likely to approve you.

- Lender comparison and product matching. Brokers access loan programs across dozens of wholesale lenders, including FHA, VA, conventional, and non-QM products. A bank loan officer can only offer that institution’s products. A broker can shop the entire wholesale market on your behalf.

- Application preparation and submission. The broker compiles your documents, prepares the loan file, and submits it to the lender portal. Errors or missing items at this stage cause delays, so an experienced broker packages the file correctly the first time.

- Underwriting advocacy. A broker’s most critical function is shaping applications to fit specific lender guidelines. Brokers know which lenders are flexible with self-employment income, recent credit events, or non-traditional assets, and they target those lenders strategically.

- Appraisal coordination. Brokers manage the appraisal process and help clients handle low appraisal challenges by renegotiating the purchase price or identifying alternative financing paths.

- Closing coordination. Broker involvement continues through closing, responding quickly to last-minute lender requests to prevent rate lock expirations or costly per-diem interest charges.

Brokers also spend significant time on compliance and regulatory documentation, a behind-the-scenes function that keeps your loan legally sound and on schedule. This administrative work is invisible to most borrowers but is one of the primary reasons loans close without surprises.

Pro Tip: Ask your broker which specific lenders they plan to approach for your file and why. A broker who can name lenders and explain their reasoning is demonstrating real underwriting knowledge, not just running a rate comparison website.

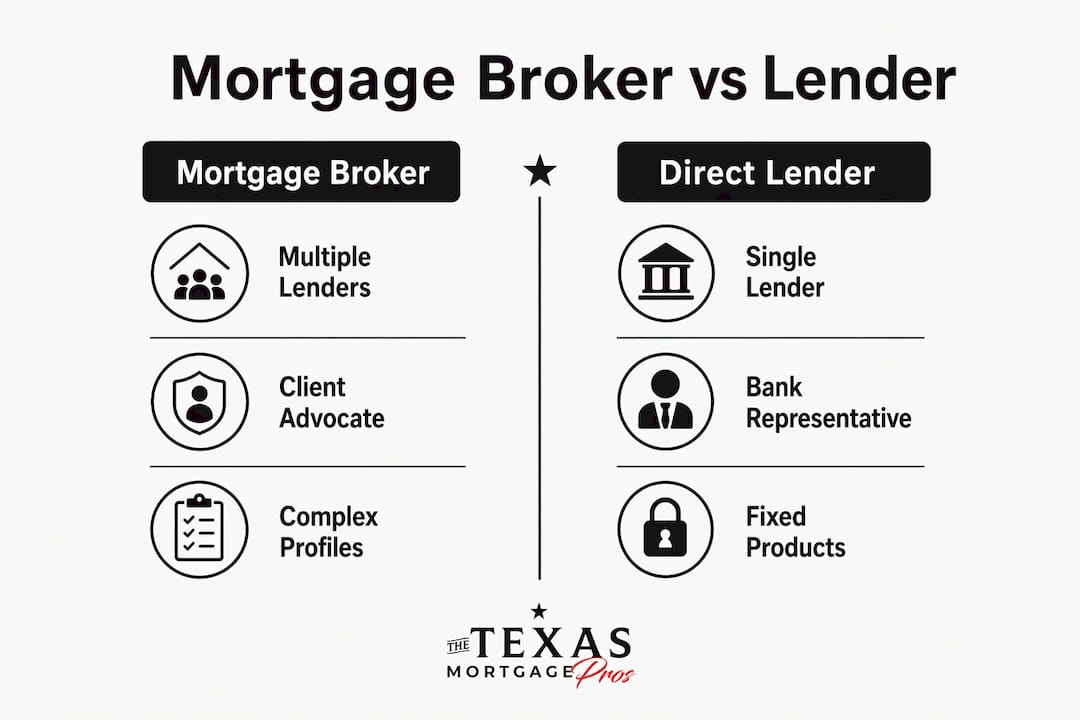

Mortgage broker vs. lender: what’s the real difference?

The core distinction between a mortgage broker and a direct lender comes down to who they work for. A bank loan officer represents the bank. A mortgage broker represents you. That difference shapes every interaction, from which products you see to how aggressively your application is packaged.

| Factor | Mortgage broker | Direct lender or bank |

|---|---|---|

| Product access | Dozens of wholesale lenders, including FHA, VA, non-QM | Single institution’s product menu only |

| Who they represent | The borrower | The lender |

| Rate negotiation | Can shop and negotiate across lenders | Fixed rate tiers within one institution |

| Complex borrower profiles | Strong fit; can match profile to flexible lenders | Limited flexibility outside standard guidelines |

| Communication | Single point of contact managing multiple lenders | Direct relationship with one institution |

| Cost | Typically lender-paid commission; sometimes borrower fee | No broker fee, but fewer options may cost more long-term |

Brokers hold a clear advantage for borrowers with complex financial profiles, such as self-employed individuals, veterans using VA benefits, or buyers with recent credit challenges. A bank will apply its own overlays and decline profiles that fall outside its narrow criteria. A broker finds the lender whose guidelines actually match your situation. For straightforward W-2 borrowers with strong credit, a direct lender can work well, but you will never know if you got the best rate without shopping the market first.

A common misconception is that using a broker adds cost. In most cases, the lender pays the broker’s commission, so the borrower pays nothing extra out of pocket. The broker’s primary advantage over a bank loan officer is advocacy. They act solely in the borrower’s interest, not the institution’s.

What are the benefits and drawbacks of using a mortgage broker?

The benefits of using a mortgage broker are most visible when your financial situation is anything other than textbook simple.

Key benefits:

- Broader loan access. Brokers work with wholesale lenders not available to the public directly. This includes non-QM loan programs designed for self-employed borrowers, investors, and those with non-traditional income documentation.

- Underwriting expertise. Brokers know which lenders accept bank statement income, recent bankruptcies, or high debt-to-income ratios. That knowledge improves your approval odds significantly.

- Time savings. Instead of applying to five lenders separately and managing five sets of paperwork, you submit once and the broker handles the rest.

- Proactive communication. Clients benefit most when brokers set clear expectations and explain trade-offs upfront, reducing anxiety throughout the process.

Potential drawbacks:

- Not every broker works with every lender. Some brokers have preferred relationships that may not include the best option for your specific profile.

- Broker-arranged loans can occasionally take longer if the broker is managing a high volume of files simultaneously.

- If you pay the broker fee directly rather than through lender-paid compensation, it affects your closing costs and should be factored into your total loan comparison.

The drawbacks are real but manageable. They come down almost entirely to choosing the right broker. A skilled, communicative broker eliminates most of these risks before they become problems.

Pro Tip: Before committing to a broker, ask how many lenders they actively work with and whether they have experience with your specific loan type, whether that is VA, FHA, jumbo, or non-QM. The answer tells you immediately whether they are the right fit.

How are mortgage brokers compensated?

Broker compensation is typically 1 to 2 percent of the total loan amount and is most often paid by the lender, not the borrower. On a $400,000 loan, that means the broker earns between $4,000 and $8,000 from the lender at closing.

| Compensation model | Who pays | Borrower impact |

|---|---|---|

| Lender-paid compensation (LPC) | The lender pays the broker | No out-of-pocket broker cost for borrower |

| Borrower-paid compensation (BPC) | Borrower pays broker fee at closing | Lower interest rate possible; higher upfront cost |

| Yield spread premium | Built into the loan’s interest rate | Borrower pays indirectly through rate |

Federal regulations, including rules under the Dodd-Frank Act, prohibit brokers from receiving compensation from both the lender and the borrower on the same transaction. This protects you from double-dipping. Brokers are also required to disclose their compensation on the Loan Estimate, so you can see exactly what they earn before you commit.

The practical implication is straightforward. When a lender pays the broker, the broker’s fee is priced into the rate offered. When you pay the broker directly, you may access a slightly lower rate. Ask your broker to show you both scenarios side by side so you can make an informed decision based on how long you plan to keep the loan. For guidance on securing competitive rates in Texas, understanding this trade-off is one of the most useful things you can do before signing anything.

Key takeaways

A mortgage broker’s value is highest when borrowers need access to multiple lenders, expert underwriting guidance, and a single point of contact managing the entire loan process.

| Point | Details |

|---|---|

| Broker as intermediary | Brokers connect borrowers to dozens of wholesale lenders, not just one institution. |

| Underwriting advocacy | Brokers match your financial profile to lenders most likely to approve your specific situation. |

| Compensation structure | Broker fees run 1 to 2 percent of the loan and are usually paid by the lender, not you. |

| Broker vs. bank | Brokers represent the borrower; bank loan officers represent the bank. |

| Closing support | Brokers manage last-minute lender requests to prevent rate lock expirations and costly delays. |

What I’ve learned about brokers that most articles won’t tell you

I have worked in mortgage lending long enough to know that the broker’s value is almost never about the rate itself. Rates are visible. Anyone can post a number on a website. What separates a great broker from an average one is what happens when something goes wrong, and something almost always does.

The appraisal comes in low. The underwriter flags a deposit. The title company finds a lien. At every one of those moments, a skilled broker already knows which lender has the most flexible guidelines, which underwriter to call directly, and how to repackage the file without starting over. That behind-the-scenes work is what clients rarely see but always feel when their loan closes on time.

I also think the industry undersells how much brokers help borrowers who do not fit the standard mold. Self-employed Texans, veterans with complex service histories, investors with multiple properties, buyers coming out of a short sale. These are the borrowers who get turned away at a bank and then discover, through a broker, that they were actually approvable all along. The mortgage broker compliance process that supports these approvals is detailed and demanding, and it is one reason why choosing a broker with real operational depth matters.

My honest advice: do not choose a broker based on a rate quote alone. Choose based on how clearly they explain your options, how quickly they respond, and whether they have handled loans like yours before. The right broker does not just find you a loan. They find you the right loan and get it closed.

Ready to find your best mortgage option in Texas?

The Texas Mortgage Pros works with a network of over 70 lenders to match Texas homebuyers and refinancers with the right loan for their situation. Whether you are buying your first home, using a VA benefit, or refinancing an investment property, we handle the lender comparison, application management, and closing coordination so you do not have to.

Use our mortgage calculators to estimate your monthly payment and affordability before you apply. When you are ready to move forward, get pre-qualified today and let us show you what competitive rates across multiple lenders actually look like for your profile. We work for you, not the bank.

FAQ

What is the role of a mortgage broker?

A mortgage broker is a licensed professional who acts as an intermediary between borrowers and multiple lenders, comparing loan products, managing applications, and supporting clients through closing. Their primary function is to find the best loan match for your financial profile across the wholesale lending market.

How does a mortgage broker get paid?

Broker compensation is typically 1 to 2 percent of the loan amount and is most often paid by the lender at closing, not the borrower. Federal regulations require full disclosure of broker compensation on the Loan Estimate before you commit.

Is a mortgage broker better than going directly to a bank?

A broker offers access to dozens of lenders and advocates solely for your interests, while a bank loan officer represents only that institution. Brokers are especially advantageous for borrowers with complex profiles, including self-employed individuals, veterans, and those with non-standard income.

What should I ask when choosing a mortgage broker?

Ask how many lenders they actively work with, whether they have experience with your specific loan type, and how their compensation is structured. A broker who answers these questions clearly and specifically is demonstrating the expertise and transparency you need.

Can a mortgage broker help with refinancing?

A mortgage broker handles refinance transactions the same way they handle purchase loans, by comparing lenders, managing the application, and coordinating closing. Refinancers benefit from the same lender comparison process that helps purchase buyers find competitive rates.