Mortgage credit score requirements are the minimum creditworthiness thresholds lenders use to decide whether you qualify for a home loan. Conventional loans generally require a minimum score of 620, while government-backed programs like FHA, VA, and USDA loans accept lower scores under specific conditions. Your score also determines your interest rate, not just your eligibility. Lenders pull a tri-merge report combining Equifax, Experian, and TransUnion, then use the median score for decisions. Knowing where you stand before you apply puts you in control of the entire process.

What are the minimum credit score requirements for different mortgage types?

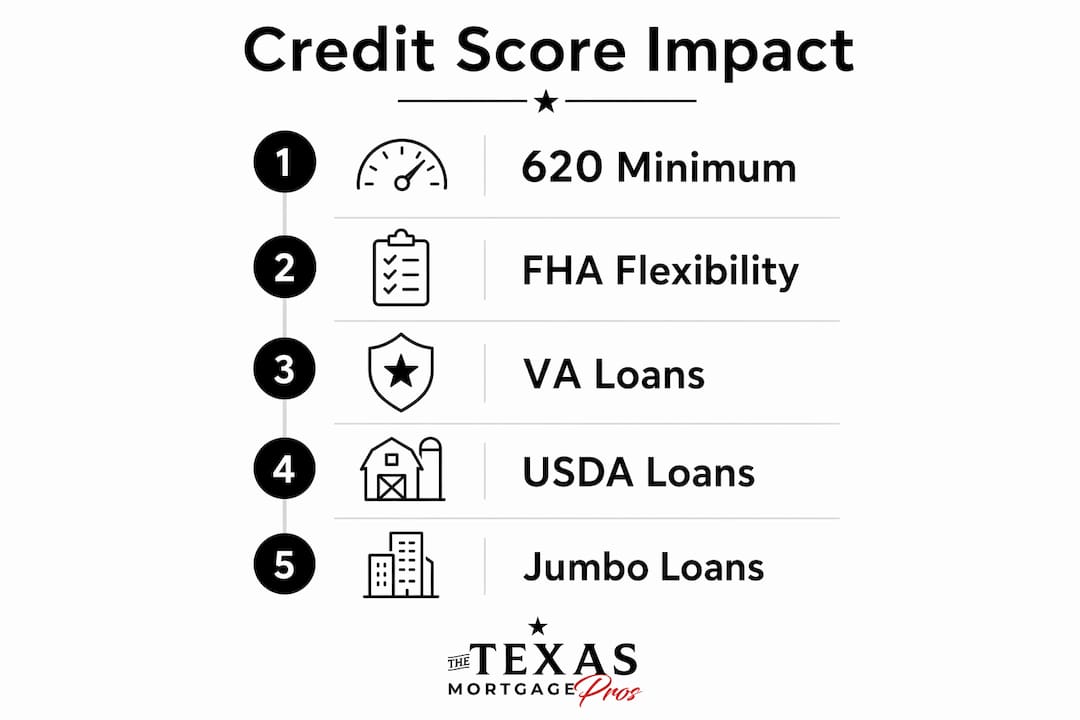

The minimum credit score needed depends entirely on the loan type you choose. Each program sets its own floor, and those floors vary widely.

Conventional loans are the most common mortgage product. They require a minimum score of 620 to qualify. Scores below that threshold will disqualify you from most conventional products, regardless of your income or down payment.

FHA loans, backed by the Federal Housing Administration, are the most forgiving option for buyers with lower scores. FHA loans accept scores as low as 500 with a 10% down payment, or 580 with just 3.5% down. That flexibility makes FHA the go-to path for first-time buyers rebuilding credit. You can learn more about how credit history interacts with FHA eligibility on The Texas Mortgage Pros FHA page.

VA loans, guaranteed by the Department of Veterans Affairs, carry no official minimum score set by the federal government. In practice, most lenders require at least 620. Veterans with scores below that threshold should shop multiple lenders, since individual underwriting standards vary.

USDA loans target rural and suburban buyers. Most lenders require a score of at least 580, and the USDA’s streamlined refinance process typically requires 640.

Jumbo loans sit above the conforming loan limits set by Fannie Mae and Freddie Mac. Because these loans carry more risk for lenders, most require scores of 700 or higher, sometimes 720.

| Loan Type | Minimum Score | Notes |

|---|---|---|

| Conventional | 620 | Standard lender requirement |

| FHA | 500 (10% down) / 580 (3.5% down) | Government-backed, flexible criteria |

| VA | No federal minimum | Most lenders require 620 |

| USDA | 580 (640 for streamlined) | Rural and suburban properties only |

| Jumbo | 700–720 | Higher risk, stricter standards |

Government-backed loans consistently offer more flexibility than conventional products. That flexibility exists because the federal government absorbs part of the default risk, which lets lenders accept borrowers who would otherwise not qualify.

How does your credit score affect mortgage interest rates?

Your credit score does more than open or close the door to approval. It directly sets the price you pay to borrow money.

Lenders treat your score as a risk signal. A higher score tells them you are a reliable borrower, so they charge less for the loan. Borrowers with scores of 740–760 or above consistently qualify for the best available rates. That matters because even a half-point difference in your rate translates to tens of thousands of dollars over a 30-year loan.

Scores in the 620–640 range face significantly higher rates and increased borrowing costs. A buyer at 620 might pay a full percentage point more than a buyer at 760. On a $300,000 loan, that gap adds up to more than $60,000 in extra interest over the life of the loan.

| Credit Score Range | Rate Tier | Typical Borrower Impact |

|---|---|---|

| 760 and above | Best available rates | Lowest monthly payment, maximum savings |

| 700–759 | Competitive rates | Modest premium over top tier |

| 660–699 | Moderate rates | Noticeable cost increase |

| 620–659 | Higher rates | Significant long-term cost |

| Below 620 | Limited options | May not qualify for conventional loans |

Small score improvements create real savings. Moving from 659 to 680 can shift you into a lower rate tier entirely. That is why credit preparation before applying is not optional. It is one of the highest-return financial moves you can make.

Pro Tip: Lower your credit utilization below 30% on all revolving accounts at least 60 days before applying. Then pull your reports from Equifax, Experian, and TransUnion through AnnualCreditReport.com and dispute any errors. Both steps can lift your score meaningfully in a short window.

What other factors do lenders consider beyond your credit score?

A credit score is one input in a larger picture. Lenders evaluate income, employment duration, and total debt obligations that your score does not capture. A strong score with weak income can still result in a denial.

The factors lenders weigh alongside your score include:

- Income and employment stability. Lenders want to see at least two years of consistent employment in the same field. Self-employed borrowers face additional documentation requirements.

- Debt-to-income ratio (DTI). This is the percentage of your gross monthly income that goes toward debt payments. Most conventional lenders cap DTI at 43–45%. A lower DTI can offset a lower credit score. Read more about how DTI affects approval on The Texas Mortgage Pros blog.

- Down payment size. A larger down payment reduces lender risk. Putting 20% down eliminates private mortgage insurance and can compensate for a borderline score.

- Cash reserves. Lenders want to see that you have savings left after closing. Two to six months of mortgage payments in reserve signals financial stability.

- Property type and loan purpose. Investment properties and second homes carry stricter requirements than primary residences.

Low credit scores are not automatic disqualification. A borrower at 600 with a 20% down payment, stable employment, and a low DTI can still close a loan. The mortgage approval process weighs all of these factors together, not in isolation. Understanding how lenders think helps you present the strongest possible application.

How can first-time buyers improve their chances of mortgage approval?

Preparation is the single biggest advantage a first-time buyer can have. Starting six to twelve months before you plan to apply gives you time to move the numbers that matter most.

- Check your credit reports for errors. Pull reports from all three bureaus and dispute inaccuracies. Correcting errors and lowering utilization can save tens of thousands over the life of your loan.

- Pay every bill on time. Payment history is the largest factor in your FICO score. Even one missed payment can drop your score significantly.

- Lower your credit card balances. Keep utilization below 30% on each card. Paying down balances is one of the fastest ways to raise your score.

- Avoid opening new credit accounts. Each application triggers a hard inquiry. Multiple inquiries in a short window signal risk to lenders.

- Choose the right loan type for your score. If your score is below 620, an FHA loan in Texas may be your best path. FHA programs pair well with down payment assistance for buyers who need help covering upfront costs.

- Explore first-time buyer programs. Texas offers several state-level programs that provide grants and low-interest second loans. The first-time homebuyer programs available through The Texas Mortgage Pros can reduce both your required score and your out-of-pocket costs.

- Shop multiple lenders. Lender overlays mean one institution may reject you while another approves you at the same score. Rate shopping within a 45-day window counts as a single inquiry under FICO scoring rules.

Pro Tip: Time your mortgage application carefully. Avoid applying for any new credit, including store cards or auto loans, for at least 90 days before submitting your mortgage application. Hard inquiry stacking in that window can drop your score by 10–20 points at the worst possible moment.

The loan approval timeline moves faster when your documents are organized and your credit is clean. Buyers who prepare early close with better rates and fewer surprises.

Key Takeaways

Mortgage credit score requirements set the foundation for loan eligibility, interest rates, and long-term borrowing costs, with scores above 740 securing the best terms and FHA loans offering the most flexibility for buyers below 620.

| Point | Details |

|---|---|

| Conventional loan minimum | A score of 620 is the standard floor for conventional mortgage approval. |

| FHA flexibility | FHA loans accept scores as low as 500, making them ideal for buyers rebuilding credit. |

| Score impact on rates | Scores of 740 and above unlock the best rates; scores below 640 carry significantly higher costs. |

| Beyond the score | DTI, income, employment, and down payment all influence approval alongside your credit score. |

| Preparation timeline | Start improving credit 6–12 months before applying to maximize your rate and loan options. |

What I have learned working with borrowers across every credit tier

The biggest misconception I see is that a low credit score is a hard stop. It is not. A FICO score above 620 is the conventional baseline, but I have worked with borrowers well below that who closed successfully through FHA programs with strong compensating factors.

What actually derails applications is last-minute behavior. Buyers who open a new credit card two weeks before closing, or who co-sign a car loan for a family member during underwriting, create problems that no amount of preparation can fix. The credit profile that gets you approved is the one you maintain consistently, not the one you patch together at the end.

The other thing worth saying plainly: the mortgage industry is still largely built on legacy FICO models. Newer scoring models like FICO 10T are coming, but lenders have not fully adopted them yet. That means the fundamentals still win. Pay on time, keep balances low, and do not chase new credit before you apply.

Early preparation is not just about hitting a minimum threshold. It is about landing in a higher rate tier and saving real money over 30 years. That is the conversation worth having before you ever submit an application.

— Michelle

How The Texas Mortgage Pros can help you qualify

The Texas Mortgage Pros works with a network of over 70 lenders to find the right loan for your credit profile, not just the easiest one to close.

Whether your score is 580 or 760, there is a loan program worth exploring. Use the mortgage payment calculator to see how your credit score tier affects your monthly payment before you apply. Texas buyers can also access down payment assistance programs that reduce upfront costs and make qualifying easier at lower score ranges. When you are ready to take the next step, get pre-qualified today and get a clear picture of what you can borrow.

FAQ

What is the minimum credit score needed to buy a house?

The minimum depends on the loan type. Conventional loans require a score of at least 620, while FHA loans accept scores as low as 500 with a 10% down payment.

Does a higher credit score guarantee mortgage approval?

No. Lenders also evaluate income, employment history, debt-to-income ratio, and down payment. A high score improves your odds and your rate, but it does not guarantee approval on its own.

How much does my credit score affect my mortgage rate?

Significantly. Borrowers with scores of 740 and above qualify for the best available rates, while scores in the 620–640 range face noticeably higher rates that increase total loan costs by tens of thousands of dollars.

Can I get a mortgage with a credit score below 620?

Yes, through FHA loans, which accept scores as low as 500 with a larger down payment. VA and USDA loans also offer flexible criteria for eligible borrowers.

How long does it take to improve a credit score for a mortgage?

Most borrowers see meaningful improvement within three to six months of paying down balances, correcting report errors, and avoiding new credit applications. Starting 6–12 months before applying gives you the best chance of reaching a higher rate tier.